Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Disclaimer: 2026 Omnibus changes to CSRD and ESRS

In December 2025, the European Parliament approved the Omnibus I package, introducing changes to CSRD scope, timelines and related reporting requirements.

As a result, parts of this article may no longer fully reflect the latest regulatory position. We are currently reviewing and updating our CSRD and ESRS content to align with the new rules.

Key changes include:

- A narrowed CSRD scope, now limited to companies with 1,000+ employees and €450m turnover

- Delays to CSRD reporting timelines, with wave 2 and 3 reports pushed to 2028/2029 in most cases

- Simplification of ESRS datapoints

We continue to monitor regulatory developments closely and will update this article as further guidance and implementation details are confirmed.

In the global fight against climate change, transparency around environmental impact is becoming a non-negotiable part of doing business.

Regulations like the EU's Corporate Sustainability Reporting Directive (CSRD) and the EU Taxonomy now require companies to incorporate sustainability data into their financial reports and ensure it passes third-party verification.

With Chief Financial Officers (CFOs) already responsible for financial reporting, this makes them perfectly positioned to take on their companies’ sustainability efforts.

By setting up systems and allocating resources to make sure sustainability data is as accurate, timely, and auditable as financial data, CFOs are not only able to meet regulatory requirements, but also push their companies to lead in sustainable business practices.

In this article, we'll explore how the CSRD is reshaping the role of CFOs, recap the directive's key requirements, and offer a step-by-step guide to help CFOs achieve CSRD compliance efficiently and effectively.

The impact of CSRD on the role of CFOs

With the introduction of regulations like the CSRD, CFOs are finding their roles expanding to encompass managing sustainability data just as they do financial data.

Finance leaders are now tasked with collecting the right data to meet CSRD reporting requirements. This means not only gathering complex ESG data from multiple internal and external sources, but also ensuring this data is accurate and of high-quality to meet the mandatory assurance process.

Another crucial part of their role is conducting a Double Materiality Assessment. This helps finance teams gauge how sustainability issues impact their company's financial health and identify investment opportunities to boost efficiency and sustainability (more on this soon).

CFOs are also increasingly taking the lead in educating and engaging stakeholders about the company's sustainability initiatives—whether to raise capital, comply with regulations, or meet consumer expectations.

This requires effective communication and collaboration across various departments to ensure transparency and accountability in sustainability reporting.

Key requirements and objectives of the CSRD

In April 2021, the EU adopted the Sustainable Finance Package to boost sustainable investments throughout Europe. The CSRD, a central element of this package, was introduced to overcome the shortcomings of the previous Non-Financial Reporting Directive (NFRD).

The European Commission found that reports often lacked crucial information that investors and other stakeholders deemed significant. The CSRD was adopted to expand the scope and detail of sustainability reporting required for EU companies.

Its primary objective is to standardize sustainability reporting to make information more reliable and comparable—ultimately directing investments towards more sustainable technologies and businesses.

Below is a summary of the CSRD's key requirements, reporting timelines, and its impact on financial reporting and disclosure.

Reporting requirements

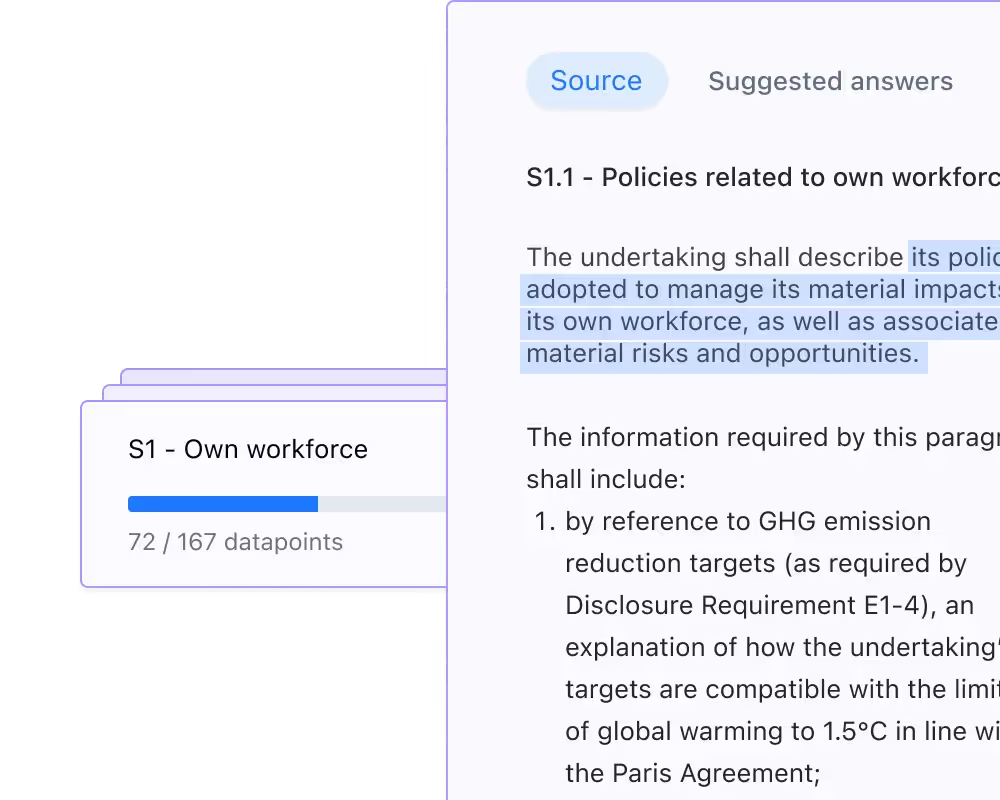

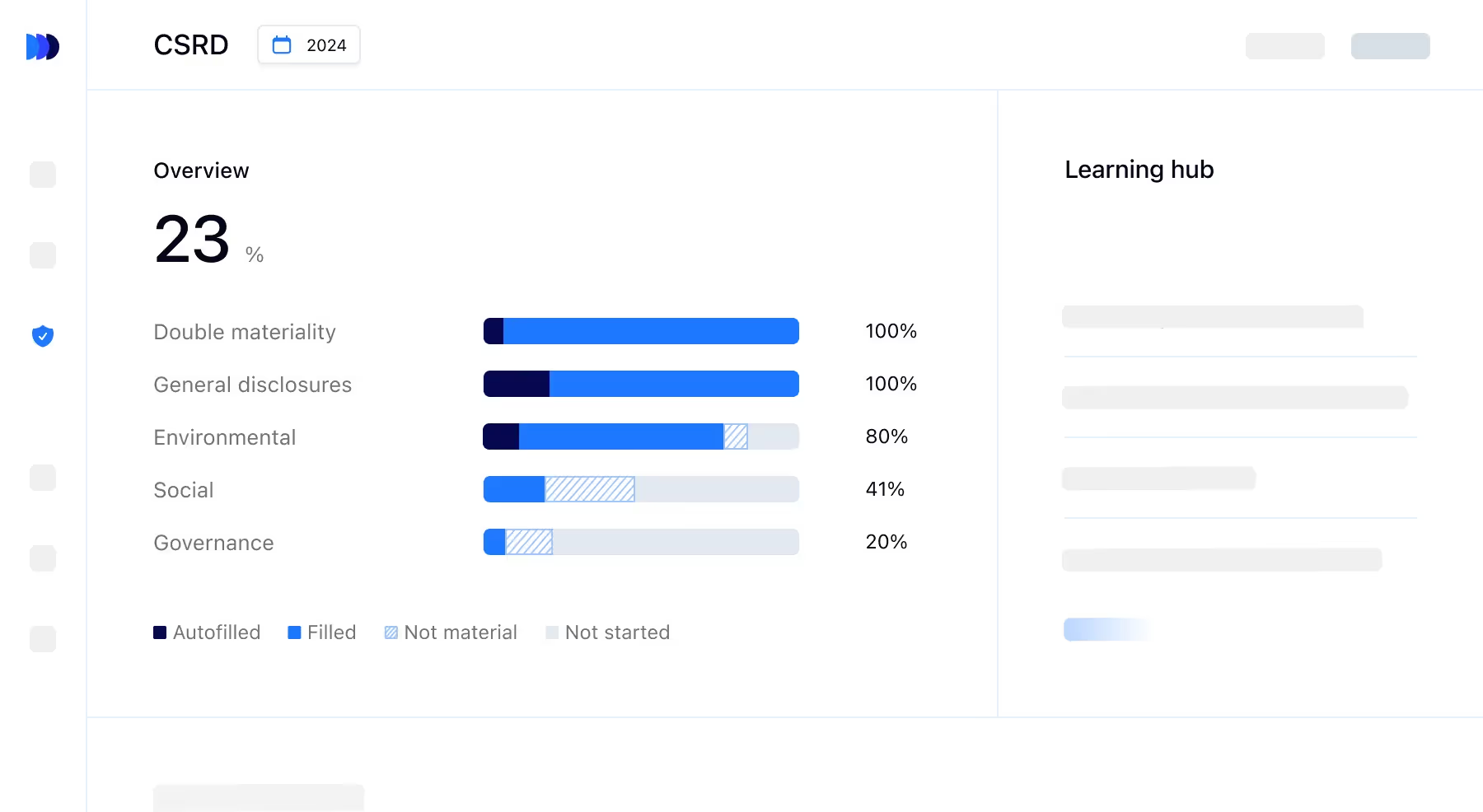

The CSRD requires impacted companies to report in line with the European Sustainability Reporting Standards (ESRS). Developed by the European Financial Reporting Advisory Group (EFRAG), these are the detailed reporting requirements companies must follow when disclosing sustainability-related information under the CSRD.

The first set of ESRS is made up of twelve standards. This includes ten sector-agnostic topical standards focusing on environmental, social, and governance (ESG) matters.

It also includes two cross-cutting standards applicable to all reporting companies. These provide general requirements for sustainability reporting (ESRS-1) and the specific disclosure guidelines for governance, strategy, impacts, risks, opportunities, and metrics (ESRS-2).

Specific standards for different sectors and mid-market companies are anticipated around mid-2026. These will provide more relevant and detailed reporting requirements for various industries as well as listed mid-market companies.

CSRD timeline

The CSRD will be phased in gradually based on company size, turnover, and location:

- 2024: Large companies currently covered by the NFRD will begin adhering to CSRD standards, with reporting starting in 2025. This means roughly 11,700 large EU-based companies will need to comply with the 12 ESRS this year.

- 2025: Large companies that meet two of these criteria—over 250 employees, more than €50 million in net turnover, or over €25 million in total assets—will need to comply with CSRD, reporting in 2026.

- 2026: Listed mid-market companies, whether small (50-249 employees, €10-50 million net turnover, €5-25 million total assets) or micro-sized (10-49 employees, €900k-10 million net turnover, €450k-5 million total assets), must start following CSRD requirements, with their first reports due in 2027.

- 2028: Third-country undertakings must start complying with the CSRD, with their reporting to begin in 2029.

Implications for financial reporting and disclosure

Here are some of the key implications of the CSRD for CFOs in financial reporting and disclosure:

- Enhanced disclosure requirements: The CSRD requires detailed reporting on how sustainability influences financial performance and operations.

- Integration of reporting: CFOs must ensure sustainability data is seamlessly integrated with financial reports, requiring strong systems for combined data management.

- Increased transparency: Companies are required to transparently disclose their sustainability strategies, policies, risks, and opportunities.

- Audit and assurance: Sustainability reports must go through independent audits to verify their accuracy and reliability.

- Strategic impact: The CSRD urges companies to no longer treat sustainability as a nice-to-have, but a core part of their business strategy.

{{custom-cta}}

What CFOs should know about double materiality and the ESRS

Not every sustainability topic covered by the ESRS needs to be included in your annual sustainability report—only those deemed “material” to your business. Conducting a Double Materiality Assessment is a crucial tool to help you identify which topics must be included.

Impact materiality and financial materiality

When performing a Double Materiality Assessment, CFOs must consider both impact materiality and financial materiality.

- Impact materiality (inside-out perspective): This refers to how your company’s actions affect people and the planet.

- Financial materiality (outside-in perspective): This refers to how sustainability issues impact your business’s financial performance and future viability.

Ultimately, double materiality is about balancing how your company influences and is influenced by sustainability issues. Evaluating your business through these two perspectives is crucial for a comprehensive and meaningful understanding of your company's sustainability performance.

6 steps for CFOs to take on becoming CSRD compliant

There are several steps finance leaders need to keep in mind when aiming for CSRD compliance:

1. Assess financial implications

Begin by evaluating the financial implications of CSRD compliance. This includes understanding the costs and resources associated with gathering, reporting, and auditing sustainability data, as well as the potential financial risks and opportunities that sustainability issues pose to the company.

2. Integrate financial reporting into CSRD data

CFOs need to ensure that their company’s financial reporting systems are aligned with sustainability data collection. This might involve updating IT systems, redefining data collection processes, and ensuring that financial and non-financial data streams are integrated in a way that aligns with CSRD guidelines.

3. Conduct a materiality assessment for financial impact

Perform a Double Materiality Assessment to determine which sustainability issues are most significant to the company’s financial health. CFOs should consider the perspectives of stakeholders and the potential financial impacts of these sustainability issues.

Unsure where to begin? We've created a free Double Materiality Assessment guide with detailed instructions on documenting and reporting your findings.

4. Integrate the revealed financial risks and opportunities into the company strategy

Once financial risks and opportunities are identified, they should be integrated into the broader company strategy. This means adjusting the company's long- and short-term goals to minimize risks and take advantage of opportunities related to sustainability.

5. Select reporting frameworks

Choose the relevant sustainability reporting frameworks that align with both the CSRD requirements and your company’s sustainability goals. This could involve adopting internationally recognized standards and frameworks that facilitate comprehensive and compliant reporting.

6. External communication and financial implications

Develop a strategy for communicating sustainability efforts and their financial implications to external stakeholders. This includes preparing clear, transparent sustainability reports that meet CSRD requirements and effectively communicate the company’s sustainability strategy, performance, and impact to investors, customers, and other stakeholders.

How much will the CSRD cost?

In November 2022, EFRAG provided a cost-benefit analysis to the European Commission detailing the estimated costs of the CSRD and ESRS reporting requirements.

For listed companies with 500+ employees

- One-off costs: EUR 395,000

- Annual recurring reporting costs: EUR 680,000

For unlisted companies with 250+ employees

- One-off costs: EUR 49,000

- Annual recurring reporting costs: EUR 85,000

Scope 1, 2, and 3 greenhouse gas emissions disclosures typically account for the majority of costs.

Currently, these estimates are based on a limited assurance requirement, but the planned introduction of stricter auditing requirements could increase expenses significantly.

It's important to update and improve your systems to better manage sustainability and long-term risks and to more accurately estimate their financial impact.

{{product-tour-injectable}}

How software can help CFOs to compliantly report

A recent EY study found that 60% of finance executives face challenges with ESG data being scattered across multiple disconnected software applications. Many CFOs are turning to specialized ESG reporting tools to centralize, standardize, and assure the accuracy of ESG data.

Platforms like Coolset are specifically designed to simplify the data collection, analysis, and reporting process.

Features like automated data aggregation, real-time analytics, and customizable reporting capabilities help CFOs make better-informed decisions and maintain compliance with ease. They also save time, cut costs, and minimize the risk of human error associated with manual reporting.

Discover how Coolset can accelerate your CSRD compliance journey by booking a free demo with one of our climate experts today.

Book a free demo with one of our sustainability experts

on mobile screens

to experience this demo.

Know your EUDR obligations

Answer a few quick questions to identify your role in the EUDR supply chain, your compliance deadline, and the exact steps you need to take. No e-mail required.

Your EUDR compliance status

Accelerate your CSRD compliance journey

Book a free demo with one of our sustainability experts