Amended ESRS explained: what changed and what companies need to report for 2026

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key Takeaways

- EFRAG's November 2025 Amended ESRS cut mandatory datapoints by 61% and remove all voluntary datapoints across all 12 standards.

- The revised standards target application from January 1, 2027, with optional early use for financial year 2026.

- Update your double materiality assessment using the new top-down approach and remove disclosures no longer required.

- Coolset helps companies apply the amended ESRS efficiently, streamline data collection, and stay CSRD-compliant.

The European Sustainability Reporting Standards (ESRS) are entering a new phase. At the end of November 2025, EFRAG submitted a simplified, reworked set of “Amended ESRS” to the European Commission, cutting mandatory data points by 61% in response to the Omnibus I Proposal.

These amended standards will now move into the Commission’s delegated act process, followed by a one-month feedback period, before becoming EU law. At this stage, the Commission is not expected to reopen the standards, but it can still introduce targeted adjustments, especially where ESRS phase-ins intersect with the ongoing debate around the future scope of Corporate Sustainability Reporting Directive (CSRD).

The following high level changes have become an integral part of the new ESRS:

- A streamlined double materiality assessment focused on “what really matters”

- Closer alignment with IFRS S1 and S2 on transition plans, financial effects and scenario analysis

- Explicit alignment with the Greenhouse Gas Protocol

- More flexibility in how companies use estimates and aggregate information

- Stronger emphasis on fair presentation rather than mandatory narrative checklists

At the same time, several disclosures become more explicit. Microplastics move out of the shadows in ESRS E2. Adequate wages are now anchored in ILO living-wage principles. Human rights policies become cross-cutting rather than siloed. And climate transition plans, while still not required, must be clearly described or explicitly acknowledged as missing.

EFRAG’s factsheet reinforces the broader intent: shorter standards, clearer language, lighter reporting burden, and smoother interoperability with ISSB.

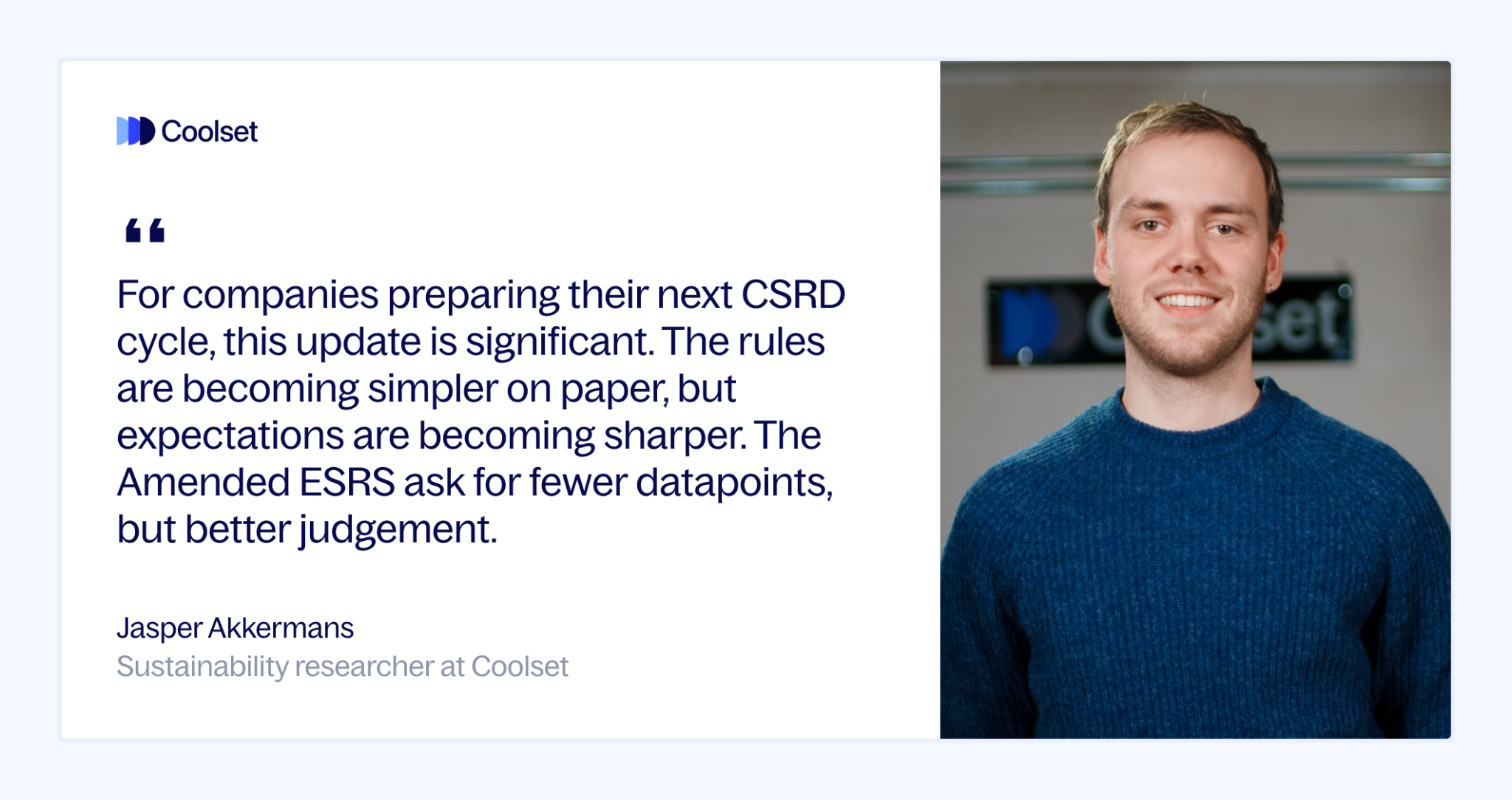

For companies preparing their next CSRD cycle, this update is significant. The rules are becoming simpler on paper, but expectations are becoming sharper. The Amended ESRS ask for fewer datapoints, but better judgement. This article breaks down what changed, what didn’t, and what it means for your reporting strategy in 2026 and beyond.

{{custom-cta}}

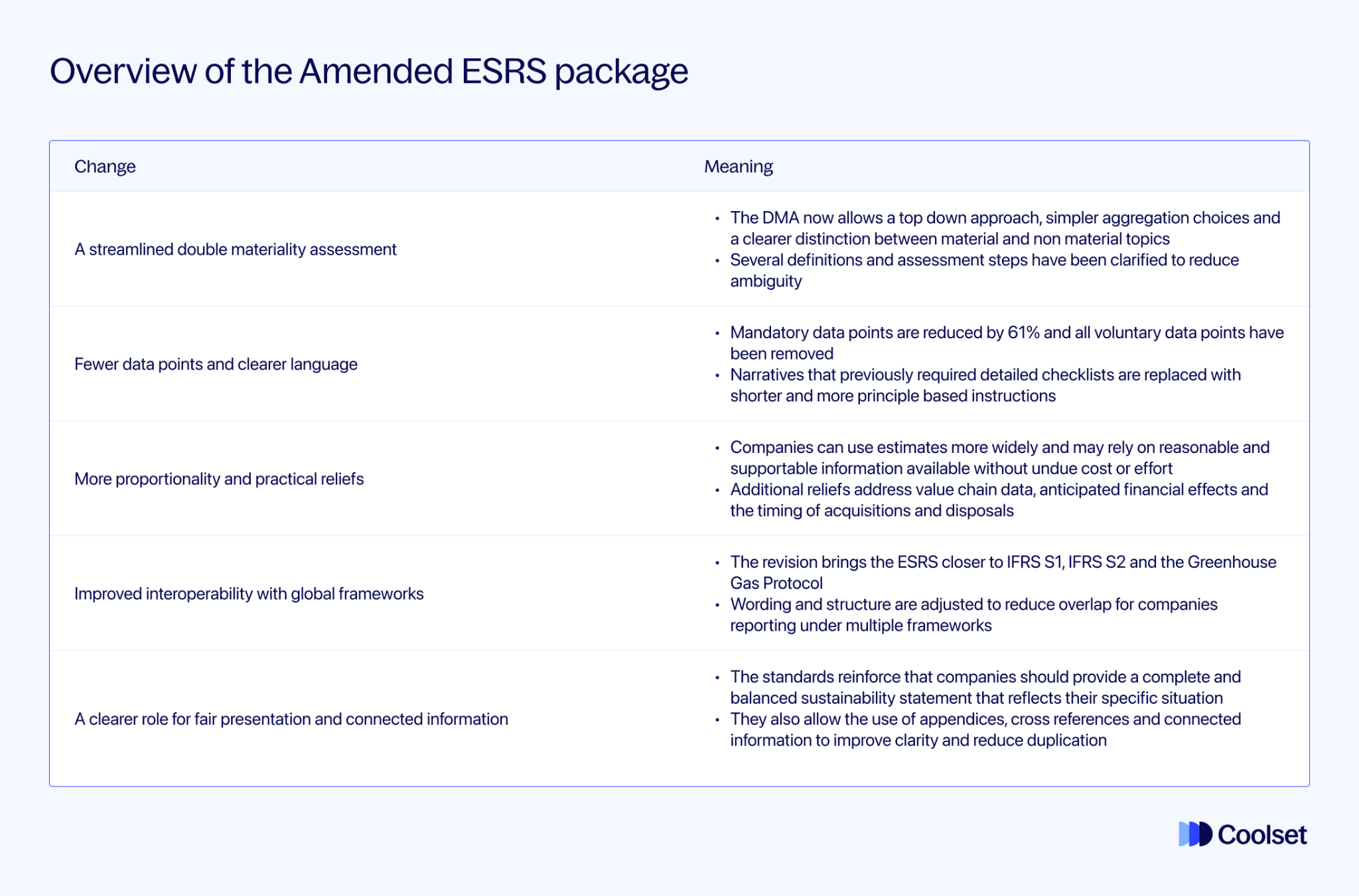

What actually changed? Overview of the Amended ESRS package

The Amended ESRS introduce a revised structure, a smaller set of mandatory disclosures and clearer guidance on how companies should approach sustainability reporting under the CSRD. The update reflects feedback from first wave reporters and aims to provide a more workable framework while keeping the original objectives of the ESRS in place.

The main themes across the package are:

- A streamlined double materiality assessment

The DMA now allows a top down approach, simpler aggregation choices and a clearer distinction between material and non material topics. Several definitions and assessment steps have been clarified to reduce ambiguity.

- Fewer data points and clearer language

Mandatory data points are reduced by 61% and all voluntary data points have been removed. Narratives that previously required detailed checklists are replaced with shorter and more principle based instructions.

- More proportionality and practical reliefs

Companies can use estimates more widely and may rely on reasonable and supportable information available without undue cost or effort. Additional reliefs address value chain data, anticipated financial effects and the timing of acquisitions and disposals.

- Improved interoperability with global frameworks

The revision brings the ESRS closer to IFRS S1, IFRS S2 and the Greenhouse Gas Protocol. Wording and structure are adjusted to reduce overlap for companies reporting under multiple frameworks.

- A clearer role for fair presentation and connected information

The standards reinforce that companies should provide a complete and balanced sustainability statement that reflects their specific situation. They also allow the use of appendices, cross references and connected information to improve clarity and reduce duplication.

Overall, the Amended ESRS reduce the volume of prescribed disclosures (by 61%) and place more emphasis on relevance, materiality and consistency across the sustainability statement.

Preparing for CSRD reporting under Amended ESRS

Reporting under the amended ESRS in 2026 requires a more deliberate and structured approach than before. The focus shifts from completing extensive disclosure lists to applying the standards correctly.

Key steps companies should follow:

1. Start with a clear view of what is in scope

First, establish which ESRS standards and datapoints remain applicable under the amended ESRS. Existing reporting structures based on earlier versions should not be reused without review, as they may include disclosures that are no longer requireds

2. Apply the revised distinction between disclosure types

The amended ESRS more clearly differentiate between mandatory disclosures, conditional disclosures, and those that depend on materiality outcomes. Companies need to explicitly identify which category each disclosure falls into before reporting.

3. Prepare double materiality using the simplified framework

Double materiality remains the entry point for ESRS reporting. The simplified framework allows a more pragmatic, top-down approach, but materiality conclusions still need to be clearly reasoned and documented.

4. Focus on relevance rather than completeness

Try to avoid overly granular or defensive reporting. We recommend to resist the tendency to disclose datapoints simply because they existed in previous ESRS versions and instead align disclosures with the amended requirements.

5. Review and clean up existing disclosures

Before drafting the sustainability statement, remove outdated datapoints and narratives that no longer apply. This helps reduce reporting volume and improves clarity.

To support this process, a consolidated overview of all amended ESRS datapoints can help teams understand what remains applicable and how the requirements are structured.

Get access to the ESRS 2026 cheat sheet here.

Breakdown of core ESRS standards: General and mandatory disclosures (ESRS 1 & 2)

ESRS 1: General requirements

ESRS 1 sets the foundation for how a company determines what belongs in its sustainability statement. The amended version streamlines this process and gives companies clearer decision points. The key highlights are:

- Materiality as the primary filter for all disclosures

- Optional top down approach to assess topics

- Flexible aggregation and geographic boundaries

- Wider use of estimates when data cannot be obtained without undue cost or effort

- Ability to omit non material disclosure requirements

- Stronger emphasis on fair presentation and clearer narrative expectations

Materiality now shapes the entire reporting process. Paragraph 23 defines material information as anything that, if omitted or obscured, “could reasonably be expected to influence” decisions by users, and paragraph 24 confirms that non material disclosure requirements do not need to be reported.

The top down option offers a practical starting point. Paragraph 27 allows companies to reach a topic level materiality conclusion using their strategy, business model and geographies, with AR 8 confirming this approach.

ESRS 1 also expands flexibility in how information is structured. AR 10 permits geographic analysis at any level relevant to the company.

Data expectations are simplified. Paragraph 32 requires only “reasonable and supportable evidence” without undue cost or effort, and AR 12 specifies that companies are “not required to perform an exhaustive search for information”. Paragraph 34 allows the use of sector or regional data for value chain analysis.

Fair presentation is reinforced. The factsheet highlights an “explicit emphasis on fair presentation”, and ESRS 1 allows the use of internal references and appendices to limit duplication.

ESRS 2: General disclosures

ESRS 2 sets out the disclosures that apply to every company, independent of which topics are material. The amended version consolidates requirements, removes duplication across topical standards and clarifies what information genuinely needs to appear in the sustainability statement. The key highlights are:

- Human rights policy moved into ESRS 2 as a cross cutting disclosure

- Streamlined strategy, governance and IRO sections

- Simplified General Disclosure Requirements for policies, actions, metrics and targets

- Clearer expectations for how companies describe engagement, remediation and key actions

- Reliefs and phase ins for anticipated financial effects

- More flexibility to avoid duplication and use internal references

ESRS 2 functions as the core set of disclosures that apply universally. The standard confirms that the information in ESRS 2 is “fundamental in nature and therefore likely to result in material information for all undertakings” (AR 11).

Governance and strategy disclosures have been reduced. The factsheet notes reduced granularity in GOV 1 and GOV 2 and less detail in SBM-1 on the business model. Engagement expectations in SBM 2 are also simplified, with focus placed on key stakeholders.

Information on impacts, risks and opportunities is now structured more clearly. SBM 3 covers how IROs interact with strategy and business model, while the detailed description of IROs themselves sits in IRO 2. Several datapoints were deleted to simplify the overall flow.

General Disclosure Requirements for policies, actions, metrics and targets (GDR P, A, M and T) have been consolidated. ESRS 2 removes overlapping instructions from topical standards and introduces a single set of narrative expectations. The factsheet mentions that these requirements were “simplified by deleting unnecessary overlap with topical standards”.

ESRS 2 also adjusts expectations around anticipated financial effects. Quantitative information remains required, but with phase ins until 2029 and additional reliefs aligned with IFRS S1.

Overall, ESRS 2 gives companies a clearer and more consistent foundation for the sustainability statement, reducing repetition and focusing attention on the information that underpins all ESRS reporting.

Environmental standards (ESRS E1-E5)

ESRS E1: Climate change

ESRS E1 sets the requirements for disclosing climate impacts, risks, opportunities and progress. The amended standard restructures the transition plan disclosure, improves alignment with IFRS S2 and the Greenhouse Gas Protocol and clarifies several key metrics. The key highlights are:

- Clearer structure for transition plan disclosures

- Alignment with IFRS S2 on assumptions, dependencies and resilience

- No obligation to have a transition plan, but mandatory disclosure if none exists

- Explicit GHG Protocol references for scope 2 and scope 3 boundaries

- Reliefs and phase ins for anticipated financial effects and difficult metrics

- Locked in emissions included explicitly

- Updated guidance on targets, 1.5 degree alignment and net zero

The transition plan disclosure in ESRS E1 sets out what a plan should cover, including targets, actions and how the plan aligns with climate neutrality. If a company has no transition plan, ESRS E1 requires a statement to that effect and an indication of whether one is expected in the future.

Disclosures on climate impacts, risks and resilience are reorganised. ESRS E1 brings these closer to IFRS S2 and confirms that scenario analysis is voluntary, while still requiring companies to explain how they assess resilience when climate risks are material.

Emissions reporting is clarified. ESRS E1 specifies the boundary for scope 1, scope 2 and scope 3 emissions and requires companies to consider the Greenhouse Gas Protocol scope 2 and scope 3 standards when preparing inventories.

Target setting is refined. ESRS E1 updates requirements around base years, maintains the expectation of 1.5 degree alignment and reintroduces net zero guidance. Reliefs and phase ins apply to anticipated financial effects, with quantitative elements not required immediately.

ESRS E2: Pollution

ESRS E2 covers emissions to air, water and soil, including microplastics and hazardous substances. The amended standard clarifies what must be measured and which companies fall under the more detailed chemical reporting requirements. The key highlights are:

- Microplastics now explicit: Quantitative disclosure for primary microplastics and qualitative for secondary microplastics

- Clearer pollutant identification: Use of E PRTR and IEPR thresholds when assessing material pollutants

- More focused SoC and SVHC metrics: Non chemical undertakings report only on SVHC; SoC reporting applies to chemical undertakings with phase ins

- Leaner requirements for policies and actions: Narrative expectations aligned with ESRS 2

ESRS E2 now includes primary and secondary microplastics directly in the E2-4 metrics disclosure. Companies must report amounts of primary microplastics manufactured, used or directly released, while secondary microplastics require qualitative information only.

For pollutants, ESRS E2 points companies to the European Pollutant Release and Transfer Register and the Industrial Emissions Portal Regulation to help determine which pollutants are material, using their threshold values as reference points.

Substances of very high concern and substances of concern are handled through E2-5. Reporting for non chemical undertakings is limited to substances of very high concern, while the broader substances of concern metric applies only to chemical undertakings and is subject to phase ins.

Policies, actions and targets in ESRS E2 now rely on the general disclosure structure in ESRS 2, which reduces repetition and narrows the narrative burden.

ESRS E3: Water

ESRS E3 sets out how companies report on water use, water related risks and water impacts. The amended standard clarifies the scope of water, sharpens the focus on stressed locations and simplifies the required metrics. The key highlights are:

- Stronger focus on areas with water stress

- Core metrics for withdrawal, discharge, consumption, reuse and storage

- Clearer definitions for water stress, water scarcity and water related risks

- Optional disaggregation where geography drives differences in impacts

- Clearer links to climate, biodiversity and social topics

ESRS E3 clarifies the scope of water by defining it to include freshwater as well as other types such as brackish water, seawater and third party water.

The standard places greater emphasis on location specific context. Methodological guidance explains how to determine whether an area is water stressed and confirms that companies should disaggregate or aggregate water information to match the geography of their impacts.

Metrics are simplified. Water withdrawal and water discharge are mandatory, supported by methodological guidance on calculation and units, while the water intensity metric is removed.

ESRS E3 also clarifies how water interacts with other ESRS topics. The standard notes that water use, climate impacts and biodiversity impacts are interconnected and must be assessed consistently, especially in high impact geographies.

ESRS E4: Biodiversity and ecosystems

ESRS E4 covers how companies report their impacts on species, habitats and ecosystems. The amended version narrows when a transition plan must be disclosed, clarifies key location based concepts and consolidates metrics. The key highlights are:

- Transition plan disclosure required only when a biodiversity plan already exists and is public

- Alignment with the Kunming Montreal Global Biodiversity Framework

- Clearer definitions of biodiversity sensitive areas and the area of influence

- Consolidated metrics focused on material biodiversity impacts

- Stronger links to climate, water and affected communities

The transition plan requirement is conditional. ESRS E4-1 applies only if the company has a biodiversity transition plan and has made its key features public. The objective is to describe how the business model aligns with the Global Biodiversity Framework.

Location concepts are clarified. ESRS E4 introduces an “area of influence” definition to determine when a site is in or near a biodiversity sensitive area, using buffer distances based on regulation, science based recommendations or industry best practice.

Metrics are streamlined. E4-5 consolidates location specific biodiversity disclosures: companies report the locations of material impacts, the related sensitive areas and the activities that drive those impacts.

Target setting guidance is strengthened. Biodiversity targets should be science based, aligned with ecological thresholds and contribute to the Global Biodiversity Framework. They may be set at site, landscape or company level depending on influence.

ESRS E5: Resource use and circular economy

ESRS E5 focuses on how companies use materials, design products and manage waste. The amended version sharpens the role of key materials, simplifies inflow and outflow metrics and adds a new transparency requirement on waste destinations. The key highlights are:

- Simplified structure built around “key materials”, now a defined concept

- Clearer disclosure of secondary (recycled and recovered) materials

- New metric on waste with an unknown final destination

- Product circularity attributes, including a designed recyclability rate

- Alignment with European Union circular economy and product rules

Key materials form the basis of resource inflow metrics. ESRS E5-4 requires companies to report material inputs by key material, replacing the previous biological and technical material categories. Secondary resources must be disclosed as total weight or percentage of total inflow.

Waste reporting is strengthened. E5-5 introduces a new datapoint for the share of waste with an unknown final destination, highlighting gaps in downstream traceability. Companies must also identify the key materials present in each waste stream.

Product circularity metrics are expanded. ESRS E5 includes a designed recyclability rate for products and packaging, based on the share of materials that are recyclable.

The standard reflects the wider European Union regulatory landscape by integrating concepts from the European Union Circular Economy Action Plan and relevant product legislation. This positions ESRS E5 as the link between resource inflows, product design and waste outcomes.

Social standards (ESRS S1-S4)

ESRS S1: Own workforce

ESRS S1 covers employment conditions, pay, dialogue and workforce wellbeing. The amended version tightens wage and pay reporting, simplifies several metrics and clarifies when disclosures apply. The key highlights are:

- Adequate wages now anchored in ILO living wage principles

- Unadjusted gender pay gap remains mandatory

- Adjusted gender pay gap becomes entity specific

- Clearer expectations for grievance mechanisms and remediation

- Streamlined workforce metrics with reduced narrative requirements

Adequate wages are now assessed using the ILO Principles for Estimating a Living Wage. ESRS S1-9 allows a choice between two methodologies for non European Union countries and requires companies to disclose the benchmark they used for transparency and comparability.

Pay gap reporting is sharpened. ESRS S1-15 keeps the unadjusted gender pay gap mandatory and clarifies how it must be calculated. The standard also confirms that an adjusted gender pay gap can be provided as entity specific information to supplement the mandatory figure.

Grievance channels and remediation expectations are consolidated across S1-S4. The factsheet explains that previous disclosure requirements on engagement, channels and remedy were merged and simplified, with several data points deleted.

Workforce metrics are streamlined. ESRS S1-5 and S1-7 use a revised significance threshold based on the ten largest countries of operation, with a de minimis of fifty employees per country. ESRS S1-6 reduces non-employee information to a single essential datapoint, applicable only when non-employees are critical to the business model.

These changes reduce unnecessary granularity while keeping the core pay, wage and worker protection metrics central in ESRS S1.

ESRS S2: Workers in the value chain

ESRS S2 addresses impacts on workers who are not employed by the company but operate in its upstream or downstream value chain. The amended standard reduces narrative load and concentrates on material human rights risks. The key highlights are:

- More focused policies and actions on upstream and downstream impacts

- Clearer expectations for grievance channels and remediation

- Stronger emphasis on alignment with UNGP and OECD due diligence standards

- Fewer datapoints, with tighter expectations where risks are material

S2 defines value chain workers broadly, including supplier employees, outsourced workers on company sites and workers deeper in the supply chain who extract or process inputs.

Policies in S2-1 require companies to explain how their policies address material impacts, including whether they cover trafficking in human beings, forced labor and child labor, and whether a supplier code of conduct is in place.

S2-2 and S2-3 combine engagement, grievance mechanisms and remediation. Companies must describe how workers in the value chain can raise concerns and how their input informs prevention, mitigation and remedy.

Targets in S2-4 can be qualitative or quantitative and must link to actions and engagement.

Across S1 to S4, the simplified ESRS social architecture merges and deletes many narrative datapoints, while clarifying that disclosures only apply where the topic is material.

ESRS S3: Affected communities

ESRS S3 addresses impacts on communities linked to the company’s operations or value chain. The amended standard tightens definitions, strengthens links to human rights frameworks and simplifies disclosures. The key highlights are:

- Clearer anchoring in international human rights instruments

- Sharper expectations for engagement with communities, including Indigenous peoples and FPIC

- Grievance mechanisms aligned with UNGP effectiveness criteria

- More precise definition of human rights incidents, with aggregation allowed

- Targets streamlined through ESRS 2

S3 applies only when affected communities are a material topic. The standard refers directly to the International Bill of Human Rights, the UN Guiding Principles and the OECD Guidelines, positioning these frameworks as the basis for identifying impacts and designing responses.

Engagement requirements in S3-2 focus on how communities participate in decision making. Where Indigenous peoples are concerned, companies must disclose how free, prior and informed consent is respected.

Grievance channels must be described, including how their effectiveness is assessed against UNGP criteria.

Human rights incidents are narrowly defined as substantiated cases linked to internationally recognized rights, with examples such as land rights or FPIC disputes. Companies may aggregate cases by type or geography rather than list them individually.

S3-4 links to ESRS 2 for targets. Targets may be qualitative or quantitative but should reflect engagement with affected communities.

ESRS S4: Consumers and end users

ESRS S4 covers impacts on people who use a company’s products or services. The amended standard reduces narrative detail, sharpens expectations for grievance channels and keeps incident reporting focused and materiality driven. The key highlights are:

- Simplified reporting on safety, inclusion and information related impacts

- Clearer requirements for grievance channels and approaches to remediation

- Streamlined narratives, with explicit incident reporting retained where material

S4 applies only when consumers or end users face material impacts. The standard mirrors the S1–S4 social architecture, with disclosures on policies, engagement and remedy, actions and targets aligned to ESRS 2.

S4-1 requires companies to explain how their policies address product or service related impacts, including safety, accessibility and responsible marketing. S4-2 combines engagement and grievance mechanisms, asking companies to describe how consumers can raise concerns and how effectiveness of remedy is assessed. These provisions reflect the simplified social structure introduced across S1–S4.

Incident reporting remains explicit. Material incidents such as misleading marketing, unsafe products or breaches of consumer rights must still be disclosed, with the concept of a “human rights incident” aligned with the clarified definition introduced across S2–S4: substantiated, linked to internationally recognized rights and assessed based on severity.

Targets in S4-4 follow ESRS 2 and may be qualitative or quantitative. They are expected to reflect engagement with consumer groups or their representatives, ensuring that actions and performance measures relate to the specific impacts identified.

Governance standard (ESRS G1)

ESRS G1: Business conduct

ESRS G1 sets expectations for ethical business practices, including corruption, bribery, supplier conduct and political engagement. The amended standard reduces datapoint volume and aligns the structure with the policies, actions and targets format used across the ESRS. The key highlights are:

- Leaner disclosures on corruption and anti bribery

- More flexibility on supplier ESG expectations and codes of conduct

- No standardised late payment metric for SMEs, with entity specific disclosure when material

- Clearer requirements for political influence and lobbying disclosures

- Reduced datapoint load overall

G1-1 to G1-3 are restructured to mirror the ESRS policies actions targets approach. This removes granular datapoints and concentrates disclosures on supplier relationships, corruption, bribery and whistleblowing while keeping them tied to material impacts, risks and opportunities.

Corruption and bribery metrics in G1-4 are clarified so companies report convictions, fines and sanctions within a clearer scope.

Political influence and lobbying disclosures in G1-5 are simplified, narrowing narrative requirements and focusing on material lobbying activities and expenditure.

Late payment disclosures are reduced. G1-6 removes the previous average time to pay metric and instead provides application guidance for entity specific reporting where late payments to small and medium sized enterprises are material.

Overall, ESRS G1 retains core transparency expectations but eliminates much of the detailed narrative reporting, allowing companies to focus on the governance practices most relevant to their business model and stakeholder risks.

ESRS implementation timeline and what might still change

The Amended ESRS are entering final stages of implementation. On 3 December 2025, EFRAG delivered its technical advice to the European Commission. The Commission will now draft a delegated act to revise the first ESRS set, run a one-month feedback process and then submit the text to Parliament and Council for scrutiny.

Current signals on timing and scope look roughly like this:

- Delegated act and feedback window: The Commission aims to adopt the revised ESRS delegated act as soon as possible and at the latest six months after the Omnibus package enters into force. External briefings expect adoption around mid 2026, with application targeted for financial years starting on or after 1 January 2027 and optional early application for 2026.

- Where the Commission might still adjust: The Commission can modify EFRAG’s text, within the Omnibus mandate. Commentary so far points to possible fine tuning where ESRS reliefs and phase ins interact with the revised CSRD scope and timelines, for example around anticipated financial effects, value chain data and some of the longer phase ins.

- Guidance and implementation support: EFRAG has already signalled that it will keep publishing implementation guidance, Q and A and interoperability material in December 2025. The interoperability guidance with IFRS S1 and IFRS S2 is expected to be refreshed after the delegated act is final, to reflect the new transition plan, financial effects and GHG alignment wording.

- First reporting year this will actually affect: The Commission currently targets application of the revised ESRS for financial years beginning on or after 1 January 2027, with voluntary early use possible for 2026. In parallel, the “stop the clock” decision delays CSRD Wave 2 and Wave 3 by two years, so:

- Wave 1 (large listed and other PIEs already under NFRD) continue to report under the current ESRS, plus the July 2025 quick fix reliefs, for 2024 to 2026, and are expected to switch to the Amended ESRS from 2027 onward.

- Wave 2 (other large EU undertakings) now first report for financial year 2027, in 2028, which is likely to be directly under the Amended ESRS rather than the original 2023 set.

- Wave 3 (listed SMEs) now first report for financial year 2028, in 2029, also under the revised framework if they remain in scope after the CSRD scope reform.

- Wave 1 (large listed and other PIEs already under NFRD) continue to report under the current ESRS, plus the July 2025 quick fix reliefs, for 2024 to 2026, and are expected to switch to the Amended ESRS from 2027 onward.

In other words, the simplifications are unlikely to change what Wave 1 has to report for 2024 to 2026, but they are very likely to define the rulebook for Wave 2 and Wave 3 first time reporters and for all reporters from 2027 onward.

Coolset helps companies apply the amended ESRS efficiently and stay CSRD-compliant.

See how CSRD reporting works in Coolset's platform below.

{{product-tour-injectable}}

FAQs

Do we need to redo the ESRS double materiality assessment for 2026?

Likely yes. The amended ESRS introduce a streamlined, top-down approach and clearer criteria. Your 2025 assessment may need updating to reflect the new definitions, aggregation options and the explicit ability to omit non-material topics.

Which ESRS datapoints remain mandatory?

Mandatory datapoints are reduced by 61%. Topic disclosures now depend on materiality, while ESRS 2 general disclosures still apply to all companies. Voluntary datapoints are removed altogether.

Is there a list of all amended ESRS datapoints?

Yes. The Coolset research team created the ESRS 2026 cheat sheet, which provides a consolidated overview of all amended ESRS datapoints. It shows how datapoints are structured across standards, articles, and paragraphs, helping companies understand what remains in scope and how the requirements apply to CSRD reporting in 2026. Access it here.

How do the new reliefs affect value-chain data?

You may use estimates, sector or regional data and rely on information available without undue cost or effort. Exhaustive searches are no longer required, easing upstream and downstream data gaps.

What does “fair presentation” require?

EFRAG emphasises a complete, balanced, connected sustainability statement. Less checklist-style detail is required, but clearer judgement and consistent documentation remain essential.

What should I prioritize for 2026?

Update your materiality assessment, review which disclosures still apply, adjust data processes for new reliefs, and align policies and metrics, especially around climate, wages, microplastics, key materials and human rights.

Find out how to set up a simplification-ready double materiality assessment that still holds up under assurance.

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

.webp)