CBAM reporting requirements: What companies need to know in 2026

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key takeaways

- CBAM certificate payments start as of 1 January, 2026. Poor data now = higher costs later.

- Importers must collect verified emissions data from suppliers and report quarterly using the EU methodology, with strict rules around default values.

- Coolset helps importers centralize CBAM reporting, engage suppliers, and forecast costs - without spreadsheet chaos.

As the EU's Carbon Border Adjustment Mechanism (CBAM) moves from its transitional phase into full implementation, understanding exactly what importers are required to report — and when — has become a critical compliance task.

This guide covers the core CBAM reporting requirements for companies importing CBAM goods into the EU, what data you need to gather, and how to prepare your team for ongoing compliance.

What is CBAM and why does reporting matter?

CBAM is the EU's mechanism for placing a carbon price on imports of certain carbon-intensive goods from countries with less stringent climate policies than the EU. Its purpose is to prevent carbon leakage — where EU companies move production abroad to avoid EU carbon costs — and to incentivize non-EU suppliers to reduce their emissions.

CBAM applies to six sectors: cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. For importers in these sectors, CBAM creates a direct financial and compliance obligation linked to the embedded emissions in the goods they import.

A useful starting point for understanding which goods fall under CBAM is the sector breakdown guide.

CBAM phases: transitional vs. definitive

CBAM is being introduced in two phases:

- Transitional phase (October 2023 – December 2025): Importers were required to submit quarterly CBAM reports covering the embedded emissions of their imports. No financial payment was required during this phase — it was designed to prepare companies for the definitive regime.

- Definitive phase (from 1 January 2026): Importers must purchase and surrender CBAM certificates corresponding to the embedded emissions in their imports. Annual CBAM declarations replace quarterly reports. Only authorised CBAM declarants can import CBAM goods.

The shift to the definitive phase also introduced important changes to scope and timelines. For the latest updates, see the updated CBAM reporting requirements guide.

Who needs to comply with CBAM?

CBAM applies to:

- EU-based importers of CBAM-covered goods

- Indirect customs representatives acting on behalf of non-EU importers

From 2026, only companies that have obtained authorised declarant status from their national competent authority can import CBAM goods. Companies that did not apply in time may face significant disruption to their import operations.

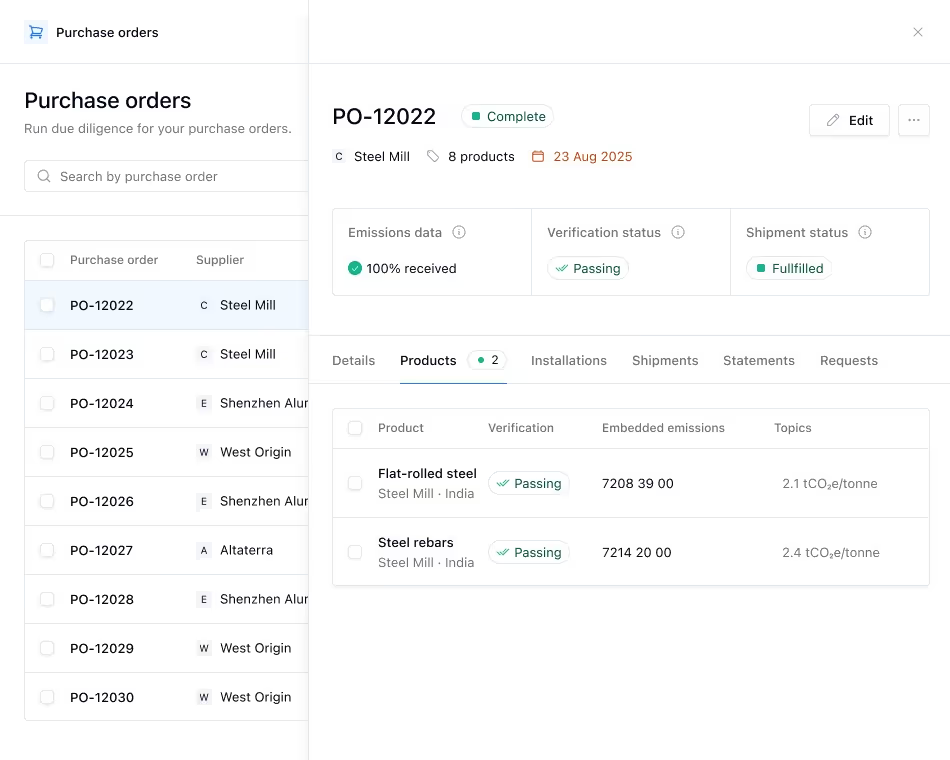

What data must importers report under CBAM?

The core of CBAM compliance is accurately calculating and reporting the embedded emissions in your imports. This requires:

- Quantity of goods imported: Volume in tonnes or MWh (for electricity)

- Country of origin: Where the goods were produced

- Embedded emissions: The direct and (for some goods) indirect greenhouse gas emissions generated during production, expressed in tonnes of CO2e per tonne of goods

- Carbon price paid: Any carbon price already paid in the country of origin, which can reduce the CBAM certificate obligation

Embedded emissions must be calculated using EU-defined default values or, ideally, actual production data supplied by the non-EU manufacturer. Using actual data (verified by an accredited third party) can significantly reduce your CBAM costs if your suppliers operate with lower emissions than the EU defaults assume.

How to calculate CBAM costs as an importer

Your CBAM financial obligation is calculated as follows:

CBAM cost = Embedded emissions (tCO2e) × CBAM certificate price (€/tCO2e) − Carbon price already paid in origin country

The CBAM certificate price tracks the EU ETS carbon price. As of 2026, EU ETS prices have fluctuated significantly, making accurate emissions data increasingly valuable for managing your import costs.

For a detailed walkthrough of the calculation methodology, see our guide on how to calculate CBAM costs.

Key steps to prepare for ongoing CBAM compliance

- Register as an authorised CBAM declarant with your national competent authority if you haven't already done so.

- Map your CBAM-covered imports by HS code and country of origin to understand your full exposure.

- Engage your non-EU suppliers to collect actual production emissions data. This is often more favourable than EU default values and can reduce your certificate costs substantially.

- Set up a data collection system to gather and store embedded emissions data from suppliers on a regular basis.

- Monitor the CBAM certificate market and consider your certificate purchasing strategy, especially as the EU ETS price can vary.

- Prepare for annual declarations under the definitive regime, which replace the quarterly reports required during the transitional phase.

How Coolset supports CBAM compliance

Coolset helps importers manage the data collection and calculation challenges at the heart of CBAM compliance. The platform supports supplier data requests, embedded emissions calculations, and audit-ready reporting — reducing the manual burden of CBAM compliance for procurement, sustainability, and finance teams.

To learn more about how Coolset can support your CBAM reporting, book a free demo.

Get a step-by-step guide to identify in-scope goods, collect supplier data, calculate costs, and set up ongoing CBAM compliance.

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

From zero to CBAM-compliant in a few weeks

Get the tools, structure and support you need to meet CBAM requirements with no prior experience or systems.

.webp)