CBAM timeline, deadlines and phases: What to expect in 2026

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key takeaways

- CBAM prices the carbon in imports of cement, steel, aluminium, fertilisers, electricity and hydrogen to prevent carbon leakage and level the playing field with EU producers.

- From 1 January 2026, importers must buy and surrender CBAM certificates annually based on verified emissions; non-surrender carries a €100 per excess tonne penalty.

- Closing supplier data gaps and building a verified cost forecast are the fastest ways to reduce 2026 certificate exposure.

- Coolset centralizes emissions data, simplifies supplier engagement, and streamlines CBAM certificate forecasting and compliance.

If you import carbon-intensive goods into Europe, chances are you’ve heard of the Carbon Border Adjustment Mechanism, also known as CBAM.

Part of the EU’s Fit for 55 package, CBAM puts a fair price on the carbon embedded in certain imported products: namely cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen.

Its goal is to prevent carbon leakage, where companies move production abroad to sidestep EU climate rules. It also helps to level the playing field between EU and non-EU producers.

CBAM reporting is already mandatory. Quarterly reporting applied from October 1, 2023 through December 31, 2025. From January 1, 2026, CBAM has entered its definitive phase: reporting shifts to an annual declaration, reported emissions must be verified and 2026 imports create CBAM certificate cost exposure.

With financial penalties and potential import restrictions for non-compliance, timing matters. This article breaks down the CBAM phases, key deadlines, and what mid-market importers should focus on in 2026.

CBAM overview: Why the two phases?

CBAM was rolled out in two phases to give businesses time to build internal systems, like mapping supply chains and collecting emissions data from suppliers, and to adapt to the new reporting requirements. It also gave the EU some time to fine-tune the framework.

As explained on the EU CBAM official website “The gradual phasing in of CBAM allows for a careful, predictable, and proportionate transition for EU and non-EU businesses, as well as for public authorities.”

From 1 October 2023 to 31 December 2025, CBAM was in its transitional phase. Importers of covered goods were required to submit quarterly emissions reports via the CBAM Transitional Registry, but no certificates were required yet.

Now, as of 1 January 2026, the definitive phase begins. Importers will need to buy and surrender CBAM certificates based on reported emissions. Reporting is now annual, with stricter verification and audit requirements.

The phased approach is designed to prevent carbon leakage without disrupting trade. It gives businesses time to prepare while aligning with EU climate goals.

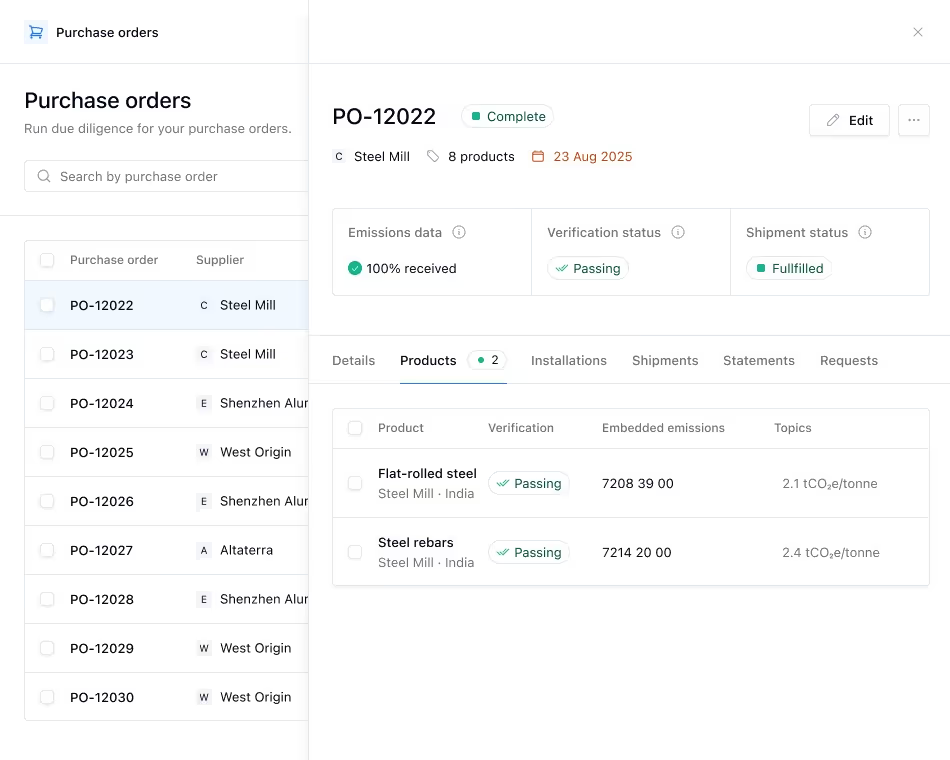

Check our CBAM certificates dedicated article to understand how to register, buy, and surrender them, plus how to forecast costs based on your emissions.

{{custom-cta}}

Key CBAM deadlines and phases: Transitional vs. definitive phase

As we’ve learnt, CBAM was structured in two phases to ease the compliance burden and allow time for adjustment, both for businesses and the EU. Here’s how the timeline breaks down:

Transitional phase (1 October 2023 – 31 December 2025)

During this period, importers of CBAM-covered goods were required to report the embedded emissions of their imports on a quarterly basis through the CBAM Transitional Registry.

Quarterly reports were due one month after the end of each quarter:

- Q1 2025: due by 30 April 2025

- Q2 2025: due by 31 July 2025

- Q3 2025: due by 31 October 2025

- Q4 2025: due by 31 January 2026

Between October 1, 2023 and June 30, 2024, companies could use default values provided by the European Commission to estimate emissions without any quantitative limit.

Starting from July 1, 2024 (Q3 2024), importers were expected to report actual emissions data, verified and calculated in accordance with the EU's CBAM methodology. For complex goods, the use of default values is limited to a maximum of 20% of total emissions reported. This requires importers to establish robust data collection processes with their non-EU suppliers well in advance of the reporting deadlines.

Importers were not required to purchase or surrender CBAM certificates during this phase.

Definitive phase (as of 1 January 2026 onward)

The definitive phase of CBAM comes into effect, requiring importers to purchase and surrender CBAM certificates corresponding to the embedded emissions of their imported goods. Reporting shifts to an annual basis, with the first report due by September 30, 2027. Third-party verification of emissions data is also now mandatory.

Failure to surrender the required number of certificates will result in a penalty of €100 per excess tonne of CO₂.

The scope of CBAM is also expected to grow. Sectors like chemicals and polymers are being considered for inclusion as early as 2027–2028, so companies importing carbon-intensive goods beyond the current list should start preparing now.

Timeline highlights: What to prepare for in each phase

Here’s what importers should prioritise now, and what to expect in the years ahead as reporting has now turned into financial enforcement.

2025: The final year of the transitional phase

Final stress-tests of emissions reporting processes before financial obligations.

Companies reliant on default values switch to actual emissions data, collected and calculated according to CBAM rules. Cross-functional coordination across procurement, sustainability, and compliance is key.

2026–2030: Transition to definitive phase

From 1 January 2026, CBAM enters its enforcement phase. This means importers must now purchase and surrender CBAM certificates annually, based on reported emissions. Third-party verification also becomes mandatory.

Use your 2025 reports to budget for 2026 certificate purchasing. Add up embedded emissions per product category, monitor EU ETS prices, and factor in any carbon prices paid abroad. This gives you a working forecast to inform budgets, pricing, and leadership decisions.

Beyond 2030: Full integration with EU ETS

CBAM is designed to gradually mirror the EU Emissions Trading System (ETS). Free allowances for domestic producers will be phased out between 2026 and 2034. Expect further regulatory alignment and potential expansions to new product categories.

Real-world scenarios

CBAM looks different for every importer. It depends on what you import, how many suppliers you manage and how quickly they can deliver installation-level emissions data.

Example 1: An aluminum importer replacing default values with supplier data

An aluminum importer has entered 2026 with supplier data gaps. A few producers still cannot provide emissions data at installation level in the EU format. The importer prioritizes the highest-volume suppliers, shares a simple template and timeline, and uses third-party support where needed so 2026 imports do not default to conservative values and inflate certificate exposure.

Example 2: A cement importer forecasting 2026 certificate costs

A cement importer needs a budget that holds up even when the EU ETS price moves. They combine 2026 import volumes with supplier-specific emissions factors, then run a low, mid and high EU ETS price scenario. This gives finance and procurement a clear view of expected certificate exposure and where switching suppliers or improving data quality would have the biggest impact.

Example 3: A fertilizer distributor getting verification-ready

A fertilizer distributor works with suppliers across multiple regions. Some suppliers have the right numbers but lack supporting evidence. The importer sets minimum documentation requirements, flags suppliers that need extra help, and lines up independent verification workflows early so the annual declaration does not turn into a last-minute cleanup.

The takeaway? In 2026, the fastest way to reduce risk is to close supplier data gaps and build a defensible cost forecast for your in-scope imports.

{{cbam-calculator-injectable}}

What happens if you miss a deadline?

Missing a CBAM reporting deadline can lead to real financial consequences.

During the transitional phase (until end of 2025), failing to submit a report or submitting incomplete data would result in national fines ranging from €10 to €50 per tonne of unreported emissions, depending on the Member State.

Now, the stakes are higher. If you don’t purchase and surrender enough CBAM certificates, you’ll face a penalty of €100 per excess tonne, with no cap.

The best way to avoid last-minute scrambling is to align early across procurement, sustainability, and trade compliance teams. Make sure supplier emissions data is collected on time and in the correct format to avoid bottlenecks at submission.

To help with the collection of this detailed information, the European Commission has provided the CBAM Communication Template for Installations.

Next steps for compliance

In 2026, mid-market importers should focus on running CBAM as a repeatable process – not a one-off compliance task. Start by confirming which imports fall under CBAM (by CN code) and what falls under the 50-tonne de minimis threshold. Then collect supplier-specific emissions data at product and installation level, aligned with the EU methodology and ready for verification.

To stay ahead of reporting obligations and future certificate costs, many companies are turning to ESG software like Coolset to centralize emissions data and simplify compliance workflows. Acting early helps reduce last-minute stress and avoid costly penalties down the line.

Need help getting CBAM-ready?

Coolset helps importers streamline emissions tracking, engage suppliers, and stay compliant, without the headaches.

How to translate CBAM reporting inputs into predictable, auditable cost exposure now

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

Get ready for CBAM

Map your imports, collect emission data from suppliers and calculate total volumes in one intuitive platform.

.webp)