What is a CBAM certificate and how do you get one?

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key takeaways

- CBAM certificates represent one tonne of CO₂-equivalent and must be purchased and surrendered annually by EU importers of carbon-intensive goods from January 2026.

- Certificate prices follow the weekly EU ETS average (currently around €70 per tonne), making early emissions tracking and cost forecasting essential.

- Importers must register as authorized CBAM declarants, collect verified supplier emissions data and surrender certificates by 31 May each year or face penalties of €100 per excess tonne.

The EU’s Carbon Border Adjustment Mechanism (CBAM) is about to enter a new phase. Until now, importers have only been required to report emissions embedded in certain carbon-intensive goods. But starting January 1, 2026, the system shifts from reporting to payment.

At the center of this shift are CBAM certificates: the currency of compliance under the new rules. Importers will need to buy and surrender these certificates to cover the embedded emissions of their imported goods.

This article breaks down exactly what CBAM certificates are, how to get them, and what your business can do now to stay ahead. We’ll cover the practical steps mid-market importers need to take, from emissions tracking to cost forecasting, to prepare for the definitive phase of CBAM.

What is a CBAM certificate?

A CBAM certificate is the unit importers will need to purchase and surrender to comply with the EU’s CBAM regulation. Each certificate represents one tonne of CO₂-equivalent emissions embedded in the imported goods.

From 2026, importers of carbon-intensive products such as cement, steel, aluminium, fertilizers, electricity, and hydrogen will need to match the emissions of their goods with CBAM certificates.

Plugging carbon leakage

The goal is to level the playing field between EU producers who already pay for their emissions under the EU Emissions Trading System (EU ETS) and foreign producers who don’t face the same carbon costs.

Without this adjustment, there’s a very real risk of carbon leakage, where companies move production to countries with weaker climate regulations, undermining the EU’s climate efforts.

In fact, according to European Parliament data, over 20% of the EU’s total CO₂ emissions are tied to goods and services produced outside the EU but consumed within it.

A carbon payment mechanism

The price of CBAM certificates will reflect the weekly average price of EU ETS allowances. This means the financial impact on importers can vary over time and will require ongoing tracking and forecasting.

For example, as of May 2025, the average EU ETS allowance price was approximately €70.38 per tonne of CO₂-equivalent. This means if you were importing goods with 1,000 tonnes of embedded CO₂ emissions, you would need to purchase 1,000 CBAM certificates, potentially costing around €70,380 at current prices.

Think of CBAM certificates as a carbon payment mechanism. While the current transitional phase focuses only on reporting, the definitive phase will bring real financial and administrative obligations. Understanding how certificates work is essential for budgeting, supplier engagement, and compliance planning.

When will you need to buy CBAM certificates?

Under the current regulation, the definitive phase of CBAM is set to commence on 1 January 2026. From this date, importers of covered goods into the EU are required to monitor and calculate the embedded emissions of their products.

Key dates:

- 1 January 2026: Start of the definitive phase; begin monitoring and calculating embedded emissions.

- 31 May 2027: Deadline for submitting the 2026 CBAM declaration and surrendering certificates, as per current regulation.

Businesses need to get ready well before 2026 by working with suppliers to access emissions data and putting systems in place to calculate and track embedded carbon accurately.

The takeaway? CBAM compliance will soon come with a real cost, and businesses that start preparing now will be better positioned to manage that cost effectively.

{{custom-cta}}

How are CBAM certificate prices determined?

CBAM certificate prices are not fixed. Instead, they’re tied to the weekly average price of EU ETS allowances. That means the cost of compliance will rise or fall with the carbon market.

Importers will need to monitor carbon prices regularly to forecast costs accurately and avoid budgeting surprises. The EU publishes the average ETS price each week, which sets the price for CBAM certificates during that period.

Non-EU carbon system examples

In some cases, importers may be able to reduce their CBAM liability if a carbon price was already paid in the country of origin. The paid amount can be deducted from the number of CBAM certificates required. But this only applies to countries with recognized carbon pricing systems. For example:

Accepted:

- Switzerland ETS (formally linked to the EU ETS)

- Norway, Iceland, and Liechtenstein (non-EU countries that participate directly in the EU ETS through the European Economic Area agreement)

Not accepted:

- UK ETS – plans to introduce its own CBAM by 2027)

- China’s national ETS – currently covers only the power sector and does not apply to industrial exports, making it ineligible for CBAM deductions

- India – lacks a nationwide carbon pricing mechanism that meets CBAM criteria

- Turkey – in the process of establishing an ETS, but it is not yet operational or linked to the EU ETS

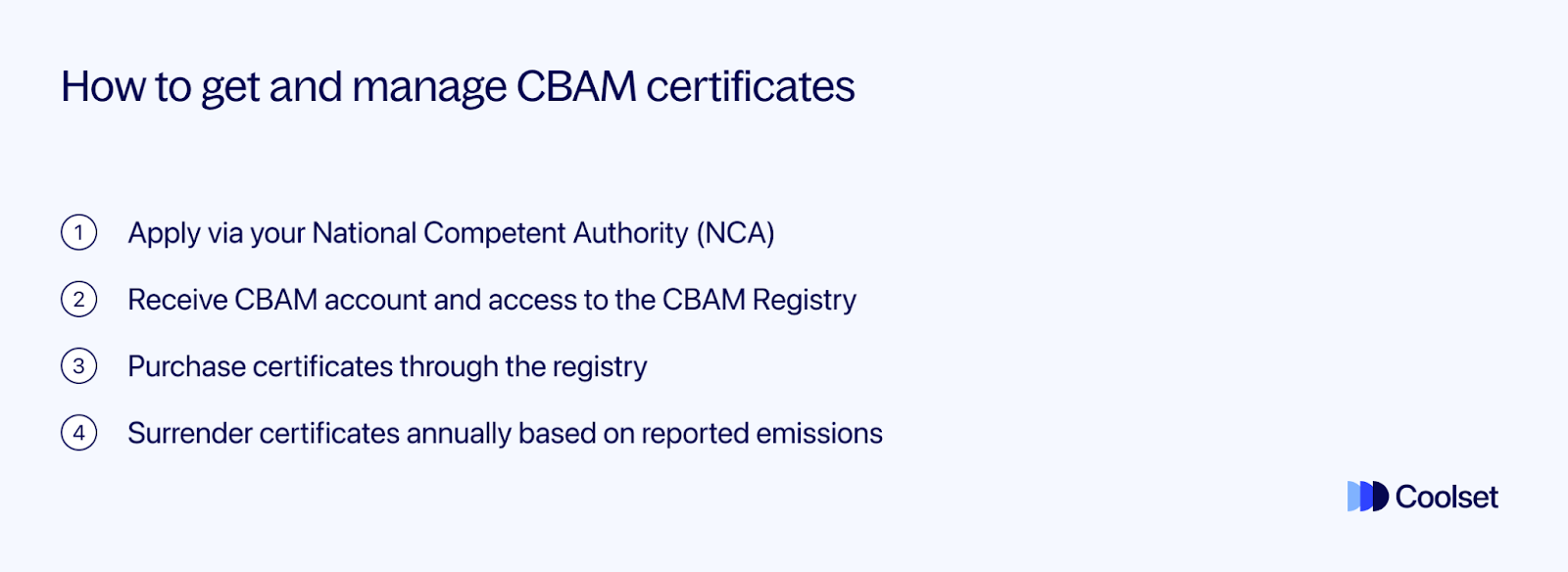

How to get and manage CBAM certificates

To purchase and use CBAM certificates, companies must first register as authorized CBAM declarants.

The European Commission opened the CBAM declarant registry on March 31, 2025, giving companies a head start on the authorization process. Without this status, you won’t be able to access the CBAM Registry or complete your obligations under the mechanism.

The process works as follows:

1. Apply via your National Competent Authority (NCA)

Each EU Member State has its own NCA responsible for approving CBAM declarants. Applications should be submitted well before the 2026 deadline to avoid delays.

2. Receive CBAM account and access to the CBAM Registry

Once authorized, companies will be issued a CBAM account in the EU-wide CBAM Registry: a central platform for purchasing, holding, and surrendering certificates.

3. Purchase certificates through the registry

You can buy CBAM certificates directly through the Registry, at the weekly price set by the EU based on the ETS average. Purchases are limited to what you need and must align with reported emissions.

4. Surrender certificates annually based on reported emissions

Each year by 31 May, importers must surrender CBAM certificates equal to the verified embedded emissions from the previous year’s imports. Importers must make sure they have the required number of CBAM certificates available on their account in the national registry.

At the end of each quarter, importers must also double-check that the number of CBAM certificates on their account corresponds to at least 80 percent of the embedded emissions in all imported goods since the start of the calendar year (see Article 19).

Be aware that CBAM certificates are also non-tradable and non-transferable. This means they can’t be resold or shared across entities, unlike EU ETS allowances, and each importer is individually responsible for compliance.

Forecasting your certificate liability

While CBAM certificate purchasing doesn’t begin until 2026, the work to forecast costs and minimize risk starts now. The key? Accurate emissions data, especially throughout 2025.

To avoid budgeting shocks, importers should begin estimating certificate volumes and costs based on the emissions data reported during the transitional phase. This means working closely with suppliers to collect embedded emissions figures regularly, rather than scrambling to gather it all at once.

Tracking emissions on an ongoing basis offers two major benefits:

- It enables gradual cost forecasting, allowing you to build your emissions liability into financial plans over time.

- It gives your company the opportunity to monitor and reduce emissions throughout the year, potentially lowering your final certificate obligation and cost.

At Coolset, we believe the smartest move now is to build a clean, consistent emissions dataset and establish regular supplier engagement. This not only smooths the path to CBAM compliance but also strengthens your broader sustainability reporting.

The earlier you start tracking, the better equipped you’ll be to control both emissions and expenses when the definitive phase hits.

Our platform helps mid-market importers forecast, calculate, and manage emissions data. Get in touch to avoid financial surprises in 2026.

{{cbam-calculator-injectable}}

Common questions about CBAM certificates

Here are some of the most common questions we hear about CBAM certificates with straightforward answers to help you prepare.

Who pays for CBAM?

Importers established in the EU are responsible for purchasing and surrendering CBAM certificates. Costs cannot be passed directly to suppliers outside the EU but may be factored into procurement strategies.

How are CBAM certificates different from EU ETS allowances?

CBAM certificates are non-tradable and non-transferable. They can only be used by the authorized declarant who purchased them. This differs from ETS allowances that can be traded across entities and markets.

What happens if I don’t surrender enough certificates?

If you fail to surrender enough CBAM certificates, you will receive a request from your competent authority to surrender the additional certificates within one month (see Article 19).

Failure to report accurately and on time can lead to fines of €10–50 per tonne of unreported emissions during the transitional phase (2023–2025). From 2026, penalties increase to €100 per excess tonne if you fail to surrender enough certificates.

Only authorized declarants can import. Unregistered companies may face stricter penalties or import restrictions.

Who is liable for emissions data accuracy?

The importing company is ultimately responsible for ensuring that emissions data reported under CBAM is accurate and verifiable even if it comes from a supplier. That’s why robust data collection and supplier engagement are essential.

Next steps

With CBAM’s definitive phase approaching, now is the time to shift from reporting to readiness. While certificate purchasing begins in 2026, the groundwork needs to happen well in advance.

Here’s what importers should focus on now:

- Register early as an authorized CBAM declarant to avoid delays

- Start collecting emissions data from suppliers regularly, not just once a year

- Model your potential certificate costs based on reported volumes and carbon intensity

The more accurate and consistent your data, the fewer surprises you’ll face, both operationally and financially, when surrendering certificates becomes mandatory.

Coolset helps mid-sized importers get CBAM-ready with emissions tracking, supplier data coordination, and compliance workflows. Request a demo today to see how we can support your CBAM compliance.

What supplier emissions data is required, where teams get stuck and how to document data for compliance

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

Get ready for CBAM

Map your imports, collect emission data from suppliers and calculate total volumes in one intuitive platform.

.webp)