How to interpret ESRS E3: Water and marine resources (Updated Mar 2026)

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

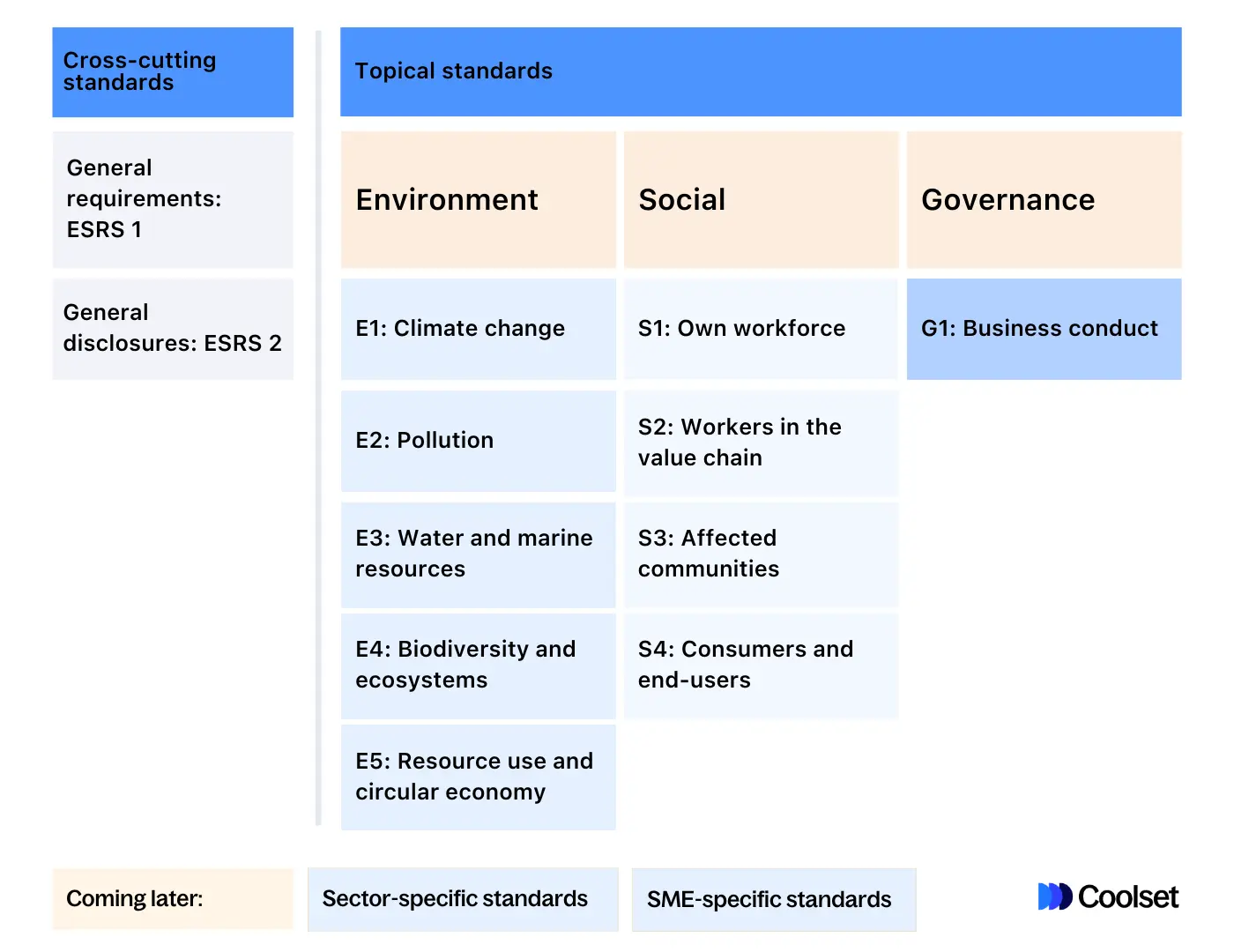

Key takeaways

- Under the simplified ESRS, E3 has been renamed to "ESRS E3 - Water" with a 70% cut in data points. Marine resource use moved to E5 and marine biodiversity to E4, leaving only freshwater and seawater use within E3's scope.

- Companies must disclose water consumption, withdrawal and discharge metrics, with mandatory reporting on high water-stress areas and recycling rates.

- Coolset's CSRD platform helps teams assess water materiality, collect E3 data points and produce audit-ready ESRS disclosures.

What is ESRS E3 exactly?

ESRS E3 focuses on water and marine resources, highlighting their crucial role in sustainability. Water conservation is essential, as global water scarcity affects four billion people a year, while pollution from industrial, agricultural, and domestic sources further degrades freshwater supplies (see also ESRS E2 on pollution). ESRS E3 encourages organizations to report on water usage, management practices, and efforts to reduce consumption and pollution, helping to address these urgent challenges.

Marine ecosystem protection is equally important in ESRS E3, given the rising threats from overfishing, pollution, and climate change. Healthy oceans are vital for biodiversity, carbon sequestration, and livelihoods, yet marine ecosystems are increasingly under stress. ESRS E3 pushes for transparency in how businesses impact marine resources, from fishing practices to wastewater discharge.

Under the simplified ESRS submitted by EFRAG in December 2025, this standard has been renamed to "ESRS E3 - Water." Marine resource use (such as fish and gravel) has moved to ESRS E5 on circular economy, while marine biodiversity and ecosystem impacts now fall under ESRS E4 on biodiversity and ecosystems. Only the use of seawater (for example, desalination) remains within the scope of E3. This represents the largest reduction of any ESRS standard: a 70.4% cut in data points and 82% reduction in word count.

What changed under Omnibus I and the simplified ESRS

The Omnibus I directive (Directive (EU) 2026/470) was published in the EU Official Journal on 26 February 2026 and entered into force on 18 March 2026. It narrows the scope of ESRS reporting to EU entities with more than 1,000 employees and more than EUR 450 million in net turnover. For a full overview of the changes, see our article on CSRD under Omnibus.

A "quick-fix" delegated act adopted in July 2025 already gave Wave 1 companies (reporting from FY 2024) a two-year postponement on phased-in E3 requirements, providing relief while the simplified standards are finalized. The European Commission must adopt the simplified ESRS as a delegated act by approximately September 2026. Companies that fall within the new scope will begin reporting under the simplified standards from financial year 2027.

The simplified ESRS also introduces a top-down materiality approach, allowing companies to predetermine the most obvious material topics based on their business model and sector before conducting a detailed assessment. The topic hierarchy has been simplified as well, with sub-sub-topics abolished. For more on how the amended ESRS affect reporting, see our dedicated article.

The ESRS E3 Disclosure Requirements

General Disclosures - ESRS 2 IRO-1

Note: Under the simplified ESRS, this disclosure is integrated into ESRS 2 General Disclosures rather than being a standalone E3 requirement.

Reporting on general disclosures of ESRS E3 requires organizations to describe the processes used to identify material impacts, risks, and opportunities (IROs). This includes outlining how water and marine resource-related risks are integrated into the overall risk management framework.

Companies should explain the criteria and methodologies applied to evaluate the significance of these impacts, such as water usage, pollution levels, or ecosystem disruptions, as well as how they prioritize actions based on these assessments.

Additionally, organizations should provide information on how their assets and activities have been screened for water and marine-related risks, detailing the tools, assumptions, and methodologies used in the process.

This disclosure should include whether consultations were conducted with stakeholders, particularly affected communities, to gather local insights and understand potential social impacts. Companies may consider frameworks like the LEAP approach to ensure comprehensive and stakeholder-informed assessments.

Impact, risk and opportunity management

Disclosure Requirement E3-1: Policies related to water and marine resources

Simplified ESRS update: Under the draft simplified standards, E3-1 is streamlined and now references the general disclosure requirement ESRS 2 GDR-P for policy disclosures.

Under ESRS E3-1, organizations must disclose their policies for managing material impacts, risks, and opportunities related to water and marine resources. These policies, as part of the Minimum Disclosure Requirements - Policy (MDR-P), are critical for addressing water use, sourcing, treatment, and pollution prevention. They also promote the design of products and services that protect marine ecosystems and reduce water consumption, especially in areas of high water stress.

Clear policies help mitigate risks, enhance sustainability, and support responsible water management across the value chain. Organizations must also disclose any policies or practices related to the sustainability of oceans and seas.

Disclosure Requirement E3-2: Actions and resources related to water and marine resources

Simplified ESRS update: Under the draft simplified standards, E3-2 is streamlined and references ESRS 2 GDR-A for action and resource disclosures.

As per the guidance in ESRS E3-2, organizations must disclose the specific actions and resources allocated to managing water and marine resources in line with their policy objectives. This disclosure clarifies how organizations aim to meet targets for water use, conservation, and ecosystem protection.

Actions and resources should be allocated toward avoiding or reducing water and marine resource usage, reclaiming and reusing water, and restoring aquatic ecosystems. Additionally, organizations must disclose any actions in high-water stress areas. These initiatives are critical for mitigating risks and ensuring sustainable water management.

Metrics and Targets

Disclosure Requirement E3-3: Targets related to water and marine resources

Simplified ESRS update: Under the draft simplified standards, E3-3 is streamlined and references ESRS 2 GDR-T for target disclosures.

Under ESRS E3-3, organizations must disclose the water and marine resources-related targets they have set to manage material impacts, risks, and opportunities. These targets support the implementation of water and marine policies and aim to improve areas such as water quality, reduce consumption, and responsibly manage marine resources.

The disclosure must specify how the targets address:

- Impacts, risks, and opportunities in areas at water risk.

- The responsible management of marine resources, including the nature and quantity of marine-related commodities.

- Reduction of water consumption, particularly in areas of high water stress.

Organizations must also report whether ecological thresholds were considered in setting these targets, including the methods used, if they are entity-specific, and how responsibility for them is allocated. Finally, they must specify if the targets are mandatory or voluntary.

Disclosure Requirement E3-4: Water metrics

Under ESRS E3-4, organizations are required to disclose their water consumption performance, focusing on material impacts, risks, and opportunities. This disclosure provides insights into the company's water use and its progress toward related targets.

Simplified ESRS update: The scope of E3-4 has been expanded under the draft simplified standards. Water withdrawal and water discharges are now mandatory metrics (previously voluntary). The standard now covers four sub-topics: water withdrawals, water consumption, water discharges, and water storage. The water intensity metric has been removed.

The disclosure must include:

- Total water consumption: The organization must report its total water consumption in cubic meters (m³).

- Water consumption in areas at water risk: This includes consumption in areas facing high water stress or other water-related risks.

- Water recycling and reuse: The volume of water recycled and reused must be disclosed, demonstrating efforts to optimize water usage.

- Water storage: The total water stored and any changes in storage should be reported.

In addition, organizations must provide contextual information on the quality and availability of water in the basins from which water is sourced, the methods used to collect data (e.g., measured, estimated, or modeled), and any standards or assumptions applied. This ensures transparency and consistency in how water-related data is gathered and assessed.

Note that under the current Set 1 ESRS, companies were also required to disclose water intensity (total water consumption per million EUR of net revenue). This metric has been removed in the draft simplified standards.

Disclosure Requirement E3-5: Anticipated financial effects from water and marine resources-related impacts, risks, and opportunities

Simplified ESRS update: This disclosure requirement has been deleted in the draft simplified standards. Anticipated financial effects are now centralized in ESRS 2, as the methodology for quantifying these effects was considered insufficiently mature for a standalone requirement.

Under ESRS E3-5, organizations must disclose the anticipated financial effects of material risks and opportunities related to water and marine resources. This information provides insights into how water and marine dependencies and impacts are expected to affect the organization's financial position, performance, and cash flows over the short, medium, and long term.

The disclosure must include:

- Anticipated financial effects of risks: Organizations must quantify or qualitatively describe the potential financial impact of material water and marine resources-related risks. This should cover how these risks could influence the entity's financial standing and cash flows.

- Anticipated financial effects of opportunities: Organizations should disclose the expected financial effects of opportunities related to water and marine resources, although quantification is not mandatory if it would compromise the quality of the information.

Additionally, the disclosure should include:

- Quantification and description: A monetary quantification of the anticipated financial effects should be provided, if feasible. If not, qualitative information should be shared. This includes details of the impacts and dependencies to which the financial effects relate and the timeframes in which they are expected to occur.

- Critical assumptions: The organization must outline the critical assumptions used to estimate these financial effects, including the sources and uncertainties of these assumptions, ensuring transparency and clarity regarding potential financial impacts.

This disclosure is designed to give stakeholders a clear understanding of how water and marine resource-related risks and opportunities could shape the organization's financial future.

Regulatory context: EU water and marine policy developments

Beyond the ESRS changes, broader EU policy developments are shaping the water and marine reporting landscape. The EU Water Resilience Strategy, adopted in June 2025, sets three goals: restoring and protecting the EU water cycle, building a water-smart economy, and ensuring clean and affordable water for all. It introduces a "Water Efficiency First" principle and extends critical infrastructure requirements to the water sector.

The European Commission has also launched a targeted revision of the Water Framework Directive (WFD) in early 2026, and a public consultation on the Marine Strategy Framework Directive (MSFD) closed in March 2026. These revisions may influence future E3 reporting expectations as the regulatory landscape continues to evolve.

Practical steps for implementing ESRS E3 Disclosure Requirements

1. Conduct a double materiality assessment

.webp)

To implement the ESRS E3 Disclosure Requirements effectively, organizations should perform a double materiality assessment which includes the sub-topics water and marine resources. Below are the concise steps for each sub-topic.

Sub-topic 1: Water

- Engage stakeholders: Consult with employees, communities, and environmental groups to gather input on water use and conservation concerns. See our guide on how to conduct stakeholder interviews for a detailed approach.

- Assess water consumption: Collect and analyze data on total water use, particularly in high-risk areas.

- Evaluate conservation efforts: Review and benchmark existing water conservation practices, identifying opportunities for improvement.

- Analyze pollution prevention: Identify pollution risks from water discharges and assess current prevention measures, implementing cleaner production techniques where necessary.

- Identify IROs: Determine the relevant impacts, risks and opportunities related to water and match them to this sub-topic.

Sub-topic 2: Marine resources

- Engage stakeholders: Collaborate with local communities, regulatory bodies, and NGOs to understand marine ecosystem health.

- Assess dependency: Analyze the organization's reliance on marine resources, identifying financial risks from changing marine resource value chains.

- Identify pollution sources: Evaluate potential pollution sources linked to marine operations and assess mitigation measures.

- Identify IROs: Determine the relevant impacts, risks and opportunities related to marine resources and match them to this sub-topic.

{{custom-cta}}

2. Set policies and targets addressing water use and marine resources

If ESRS E3 is determined to be material, corresponding policies should be defined. A sustainable water use policy should aim to reduce overall water consumption by setting specific, measurable targets, such as a [X]% reduction over [Y] years.

This policy must prioritize water recycling and reuse, striving to increase recycled water use to [Z]% of total consumption by a specified date. Implementing water-efficient technologies and practices, such as low-flow fixtures and advanced irrigation techniques, is essential for enhancing water efficiency across all operations. Furthermore, organizations must establish protocols for minimizing water pollution by adopting best practices in wastewater management, ensuring compliance with local regulations, and conducting regular employee training on water conservation techniques.

In addition, a marine resources conservation policy should focus on protecting marine ecosystems and promoting sustainable management practices. This involves committing to sourcing marine resources exclusively from sustainable fisheries and certified suppliers, thereby minimizing ecological impacts. Organizations should also implement measures to protect marine biodiversity through habitat conservation programs and partnerships with environmental organizations.

3. Select the right ESG software for water and marine resource management

To enhance compliance with ESRS E3 requirements, organizations should implement advanced tools and software for efficient data collection, analysis, and reporting on water and marine resources.

By automating data processes and integrating analytics, organizations can make informed, proactive decisions that improve water management practices and support sustainability goals, ultimately simplifying the reporting process and enhancing transparency. Coolset helps users achieve CSRD compliance by simplifying the reporting process and enhancing transparency in reporting data points. Try out our software below, or book a demo here.

{{product-tour-injectable}}

Written by our sustainability researchers, this guide contains all the steps for compiling your own DMA.

.avif)

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

.webp)