CSRD under Omnibus: updated scope, timelines, and what companies should do in 2026

.webp)

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key takeaways:

- The EU Omnibus package significantly changes the scope, timelines, and how much reporting effort is required for the CSRD.

- Aligning early with the Amended ESRS helps teams avoid over-preparing against outdated disclosure lists and focus on defensible materiality and evidence.

- Coolset supports this transition by helping teams run materiality, scope ESRS datapoints, and keep evidence audit-ready in one platform.

Corporate Sustainability Reporting Directive (CSRD) preparation plans built in 2023 and early 2024 are no longer fully fit for purpose. Since then, the EU has introduced the Omnibus package, adopted the stop-the-clock delay, signalled a narrower CSRD scope and Amended the European Sustainability Reporting Standards (ESRS). For many companies, this has created uncertainty: are we still in scope, do we still need to prepare, and what actually matters in 2026?

This guide is designed to answer those questions clearly. It explains how Omnibus changes CSRD scope and timelines, what happens to Wave 2 and Wave 3, and how teams should adjust their preparation plans for 2026.

What is the Omnibus package and how does it change CSRD reporting plans?

The Omnibus package is part of a broader EU initiative to simplify sustainability regulation and reduce unnecessary administrative burden, while keeping the core objectives of transparency and accountability intact. Reducing the administrative burden for companies is a key focus for the Commission by 25% overall and 35% for SMEs, as it will unlock billions in investment capacity.

In December 2025 the European Parliament voted in favour of the “Omnibus I” legislative package, which introduces significant changes to existing EU sustainability laws, including the CSRD. Rather than replacing the CSRD, Omnibus introduces targeted changes to how the directive applies in practice.

The Omnibus package affects the CSRD in three key ways:

- First, it narrows the group of companies that fall under mandatory reporting.

- Second, it adjusts the timing of reporting through the stop-the-clock measure, which delays when certain companies need to publish their first CSRD report.

- Third, it sets the direction towards simplified reporting with the Amended ESRS published by EFRAG.

Omnibus does not remove CSRD as a legal requirement. Double materiality remains central, sustainability information will still be subject to third-party assurance, and companies in scope will still need structured, auditable disclosures. What Omnibus changes is who needs to do this, when they need to do it, and how heavy the reporting burden is expected to be.

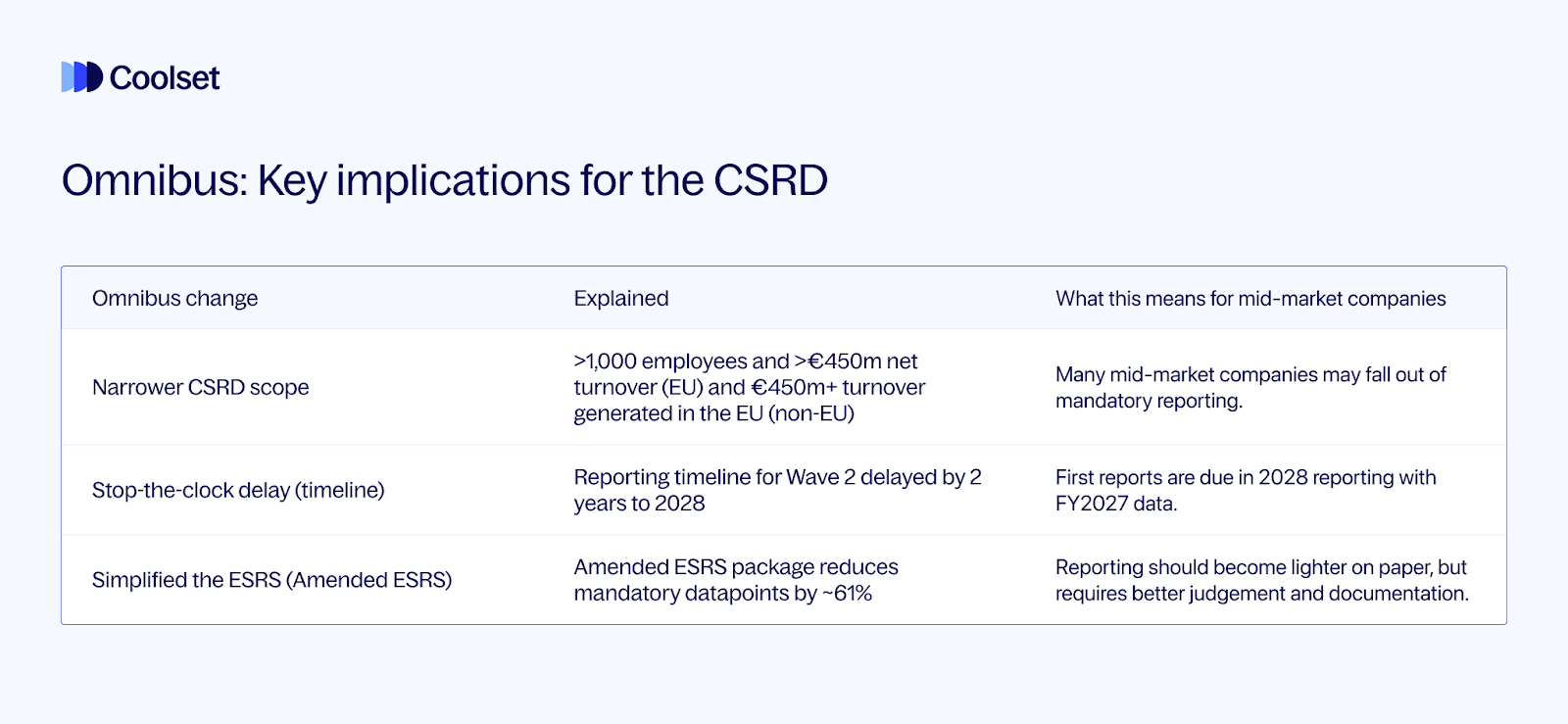

Omnibus narrows the group of companies that fall under mandatory reporting

Under the Omnibus approach, mandatory CSRD reporting is expected to apply mainly to EU undertakings with more than 1,000 employees and more than €450m net turnover, with a similar €450m turnover generated in the EU trigger for non-EU groups.

This represents a significant shift away from the original CSRD expansion, which would have captured a much broader set of mid-market companies.

For many organisations that were preparing for CSRD under the earlier thresholds, the immediate task in 2026 becomes reassessing whether CSRD remains a legal obligation or whether reporting work is now driven primarily by customer, bank, and value-chain expectations rather than by direct regulatory requirements.

CSRD-aligned reporting may still be relevant for companies outside mandatory scope, as customers, banks, and value-chain partners increasingly request comparable sustainability data to meet their own obligations.

Omnibus adjusts the timing of reporting through the stop-the-clock measure

The stop-the-clock measure that adjusts the time of reporting has already been formally adopted. For Wave 2 companies, this introduces a two-year delay to their first CSRD report. Instead of publishing in 2026 for the 2025 financial year, these companies are now expected to publish their first CSRD report in 2028, covering FY2027.

In practical terms, this turns 2026 into a preparation year rather than a reporting year. Teams can use this time to clarify scope, refresh double materiality assessments, and align internal processes with the updated direction of the standards, rather than rushing to meet deadlines that no longer apply.

Omnibus sets the direction for how reporting will be done through the Amended ESRS

In response to the Commission’s mandate, EFRAG has delivered a streamlined set of Amended ESRS, reducing datapoints by 61% (under the final EFRAG updates) compared to the original standards and placing greater emphasis on materiality and judgement.

{{custom-cta}}

While these Amended ESRS are still moving through formal adoption, they signal a clear shift in expectations. Reporting under CSRD is becoming less about completing long disclosure checklists and more about applying robust judgement. A well-documented materiality assessment, clear explanations of why certain topics are in or out of scope, and an audit-ready evidence trail will matter more than breadth of coverage.

Taken together, these three changes reshape CSRD planning. These three changes shift CSRD planning from a one-size-fits-all, to a targeted approach where companies confirm scope and timing, then scale ESRS work to the fewer datapoints while strengthening judgement and evidence.

CSRD timelines under Omnibus: what happened to Wave 2 and Wave 3?

Under Omnibus, the CSRD rollout has effectively been reshaped in two ways: Wave 2 has been delayed by the adopted stop-the-clock measure, and the original Wave 3 category is expected to fall out of mandatory scope.

Wave 1

First, it is important to mention that Wave 1 remains unchanged. These companies were already subject to the Non-Financial Reporting Directive (NFRD) and in practice this includes large EU listed companies and other public-interest entities such as certain banks and insurers. Their first CSRD reports were published in 2025, covering FY2024.

Wave 2

For Wave 2, the adopted stop-the-clock measure introduces a two-year delay. Companies that were originally expected to publish their first CSRD report in 2026 (covering FY2025) are now expected to publish in 2028, covering FY2027. This changes how teams should plan 2026: for many, it becomes a year to confirm scope, update double materiality work, and build data and evidence processes, rather than a year focused on producing a full report.

Wave 3

For Wave 3, which originally applied to listed SMEs, the Omnibus direction is that these companies are expected to be removed from mandatory CSRD reporting. Instead, the policy shift encourages voluntary reporting using a simplified framework based on VSME, especially to support common requests from customers, lenders, and larger value-chain partners.

CSRD vs ESRS under Omnibus: what changes first in practice?

CSRD and ESRS solve different problems, and Omnibus affects them in different ways. CSRD is the legal framework that determines who needs to report and when. ESRS is what teams work with day to day: the disclosure structure, the datapoints, and the evidence expectations that shape your reporting workload.

The stop-the-clock delay and scope narrowing change the regulatory timeline, but they don’t change the core work involved in getting ready. Most of the effort sits in ESRS-driven activities such as defining what’s material, translating that into the right disclosures, assigning owners, collecting data, and keeping an evidence trail that can stand up to assurance. That’s why the ESRS changes tend to show up first in practice.

Under Omnibus, EFRAG has developed Amended ESRS that cut datapoints significantly and put more weight on materiality judgement and documentation. The practical implication is that teams get more leverage from tightening materiality and building a clean evidence trail than from trying to pre-collect every datapoint from older ESRS lists. This also helps companies that are delayed or potentially out of scope stay responsive to customer and lender requests without overbuilding a full CSRD reporting machine.

Read Coolset’s detailed breakdown of the Amended ESRS.

What to do next in 2026: two realistic preparation tracks?

Most teams don’t need a full CSRD reporting program in 2026. What makes sense depends on whether you’re clearly in scope under the Omnibus direction, or likely delayed or out of scope but still getting CSRD-style requests.

Track one: You remain in scope

Focus on the work that will still matter when reporting starts.

- Clarify your CSRD status and reporting entity - Confirm whether you’re reporting at group level, and which entities need to be covered.

- Run a clear, defensible double materiality assessment - Keep the output decision-ready: what’s material, what’s not, and why.

- Turn material topics into an ESRS datapoint plan - Start from material topics, map to the relevant ESRS disclosures, assign owners, and set a realistic collection cadence.

- Build an assurance-ready evidence trail as you collect data - Capture sources, calculations, assumptions, and review steps as you go so assurance becomes validation, not reconstruction.

Track two: You are delayed or may fall out of scope

Stay prepared without overbuilding.

- Build a minimum viable reporting backbone - Prioritize the metrics and narratives that come up most often in procurement, lending, and customer requests.

- Keep materiality and key datapoints up to date - A light-touch materiality refresh and a small set of tracked datapoints keeps you responsive and reduces rework if you re-enter scope later.

- Document methods and evidence for the data you do provide - Even outside CSRD, credibility depends on being able to explain where numbers came from and how they were calculated.

Explore how Coolset helps you run materiality, collect ESRS datapoints, and keep evidence audit-ready in one platform.

Request a free demo with the team.

FAQs

Below are the answers to the most frequently answered questions on the CSRD and Omnibus. Coolset has also published a detailed Q&A article on the EU Omnibus here.

- What are the CSRD Omnibus thresholds and who is affected?

Under Omnibus, mandatory CSRD reporting is expected to apply mainly to the largest companies. In practice, this covers EU companies with more than 1,000 employees and over €450m net turnover, and non-EU groups with over €450m turnover generated in the EU. Many mid-market companies originally preparing for CSRD are likely to fall out of scope.

- What is the CSRD Omnibus timeline?

Omnibus includes a fast-tracked “stop-the-clock” measure, which has already been adopted and delays CSRD start dates for Wave 2 companies by two years. Wave 2 first reports move to 2028, covering FY2027. The wider Omnibus package, including scope narrowing and simplified ESRS, is expected to apply after final EU publication and national implementation.

- What happens to CSRD Wave 2?

Wave 2 companies no longer need to report in 2026. Their first CSRD report is now expected in 2028, covering the 2027 financial year. For most Wave 2 teams, 2026 becomes a preparation year, focused on materiality, scoping, and data readiness rather than full reporting.

- What happens to CSRD Wave 3?

Under the Omnibus direction, the original Wave 3 population (listed SMEs) is expected to be removed from mandatory CSRD scope. Instead, these companies are encouraged to use a voluntary reporting standard based on VSME to respond to customer, bank, and value-chain data requests.

- CSRD vs ESRS: what’s the difference?

CSRD is the EU law that sets who must report and when. ESRS are the reporting standards that define what must be disclosed. EFRAG has developed a simplified set of ESRS under Omnibus, and these amended standards are now with the Commission and expected to be formally adopted later in 2026.

A practical session on the amended datapoints, materiality and audit-ready reporting

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

.webp)