What is the CSRD Directive adopted by the EU and who is in scope?

.webp)

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key takeaways:

- CSRD is already in force for Wave 1 and Wave 2 first reports have shifted to 2028, covering FY2027 due to Omnibus.

- The scope for mandatory CSRD compliance is also narrowing under Omnibus.

- The Amended ESRS reduce datapoints and make materiality and evidence more critical.

- Coolset helps teams run materiality, collect ESRS datapoints, and stay audit-ready in one platform.

The Corporate Sustainability Reporting Directive (CSRD) is the European Union (EU)’s legal framework for corporate sustainability reporting. It sets out which companies must report sustainability information, what they must disclose, and how that information must be prepared, verified, and published. The CSRD replaces and expands the EU’s earlier reporting regime, the Non-Financial Reporting Directive (NFRD), by making sustainability disclosures more consistent, comparable, and decision-useful for investors and other stakeholders.

At the centre of the CSRD is a set of standards called the European Sustainability Reporting Standards (ESRS). These standards define the topics and disclosures companies must report across environmental, social, and governance (ESG) areas. Practically, the CSRD sets the legal obligation and scope for sustainability reporting, and the ESRS provide the requirements companies must follow.

The CSRD also introduces key requirements that shape how sustainability reporting is done in practice, including:

- Double materiality: companies must report both how sustainability issues affect the business and how the business affects people and the environment

- Assurance: reported sustainability information must be checked by an independent assurance provider (phased in, starting with limited assurance)

- Digital reporting: disclosures must be prepared in a digital format and tagged for machine readability

In 2025, the European Commission launched the Omnibus Proposal to simplify EU sustainability rules, including CSRD and ESRS. Some changes are already confirmed, including the legally adopted “stop-the-clock” delay. Further changes are still awaiting final legal adoption, publication, and national implementation may still introduce nuances.

CSRD timeline in 2026: who reports when?

The CSRD is being rolled out in waves, with reporting requirements introduced gradually depending on company size and listing status. The Omnibus Proposal, launched in early 2025, includes a legally adopted “stop-the-clock” directive that delayed Wave 2 reporting start date by two years. Alongside that, Omnibus also introduces broader changes to CSRD scope and ESRS reporting requirements. The change of the scope of CSRD is effectively agreed through trilogue, while the simplified ESRS are moving through the Commission delegated act process, with approval expected around summer 2026.

See our breakdown of the entire CSRD timeline below:

- 26 February 2025: European Commission proposes Omnibus I - a “simplification” package to amend CSRD (and related rules), including changes to scope, timelines, and reporting burden.

- 3 April 2025: European Parliament adopts the “stop-the-clock” proposal - Parliament votes to delay the application dates of CSRD requirements for wave 2 companies.

- 14 April 2025: Council gives final green light to stop-the-clock - The Council formally approves the stop-the-clock directive, giving legal certainty on the two-year delay for Wave 2 entry.

- Late November 2025: Trilogue negotiations open - Parliament and Council enter final negotiations on the Omnibus package text.

- 9 December 2025: Provisional agreement reached - Parliament and Council reach a political deal that significantly narrows CSRD scope and confirms the push to simplify ESRS.

- The deal narrows the CSRD scope to EU companies with >1,000 employees and >€450m net annual turnover, and to non-EU companies with >€450m turnover generated in the EU.

- Coolset provides an overview of all updated ESRS datapoints based on the December updates published by EFRAG.

- 16 December 2025: European Parliament formally approves the deal - Parliament approves the agreement as one of the final legislative steps; final approval by member states is expected in early 2026.

- January 2026: Final adoption steps still pending - The scope-narrowing elements of Omnibus are politically agreed and highly likely to be adopted, but still require final legal adoption and publication before becoming fully binding EU law. National implementation may introduce additional nuances, so companies close to the thresholds should monitor developments closely.

What are the CSRD waves?

CSRD reporting is phased in through waves based on whether a company was already covered by the NFRD, whether it qualifies as a large undertaking, and whether it is a listed SME.

Wave 1 - companies already under NFRD (reporting has started)

Who: Large listed companies and other public-interest entities that were already required to report under NFRD (e.g., certain banks and insurers).

First CSRD report published: 2025

Covers financial year: FY2024

Standards: Current ESRS (with early phase-in reliefs).

Wave 2 - other EU undertakings

Who: EU companies with more than 1,000 employees and more than €450m net annual turnover (and non-EU companies with more than €450m turnover generated in the EU).

Original first report: 2026 (FY2025)

Updated first report (after stop-the-clock): 2028

Covers financial year: FY2027

Important 2026 note: whether a company remains in scope for Wave 2 may depend on the final outcome of Omnibus scope reform. Companies close to the expected new thresholds should monitor updates.

Wave 3- listed SMEs + certain financial institutions

Who: Listed SMEs (and certain smaller financial institutions like small non-complex credit institutions and captive insurers).

Original first report: 2027 (FY2026)

Updated first report (after stop-the-clock): 2029

Covers financial year: FY2028

Important 2026 note: Under the Omnibus agreement, listed SMEs are expected to no longer fall under mandatory CSRD reporting. Instead, the European Commission is promoting voluntary reporting using the VSME standard (a simplified framework designed for SMEs).

How does Omnibus affect CSRD?

Omnibus is the EU package that resets CSRD in practice by shrinking who has to report, pushing back Wave 2 timelines, and simplifying the ESRS disclosures. It has already delayed Wave 2 reporting, confirmed a narrower scope in trilogue, and is finalising simplified ESRS via Commission approval expected in summer 2026.

Omnibus does not repeal the CSRD, but it materially changes how it will apply in practice. Supporters (including the European Commission and several member states) describe it as a simplification package to reduce administrative burden and improve competitiveness. Critics, including NGOs, trade unions, and some governments, argue it amounts to a deregulatory rollback that weakens corporate accountability and sustainability ambition.

The EU’s Omnibus reform package has introduced major changes to how CSRD is expected to work in practice over the next few years, particularly around who is in scope, when companies need to report, and how detailed the ESRS disclosures will be.

Note: The broader Omnibus scope and ESRS reforms are not yet fully finalized in law as of January 2026. The political direction is clear, but final legal adoption, publication, and national implementation could still affect details.

Below are the three most important ways Omnibus affects the CSRD:

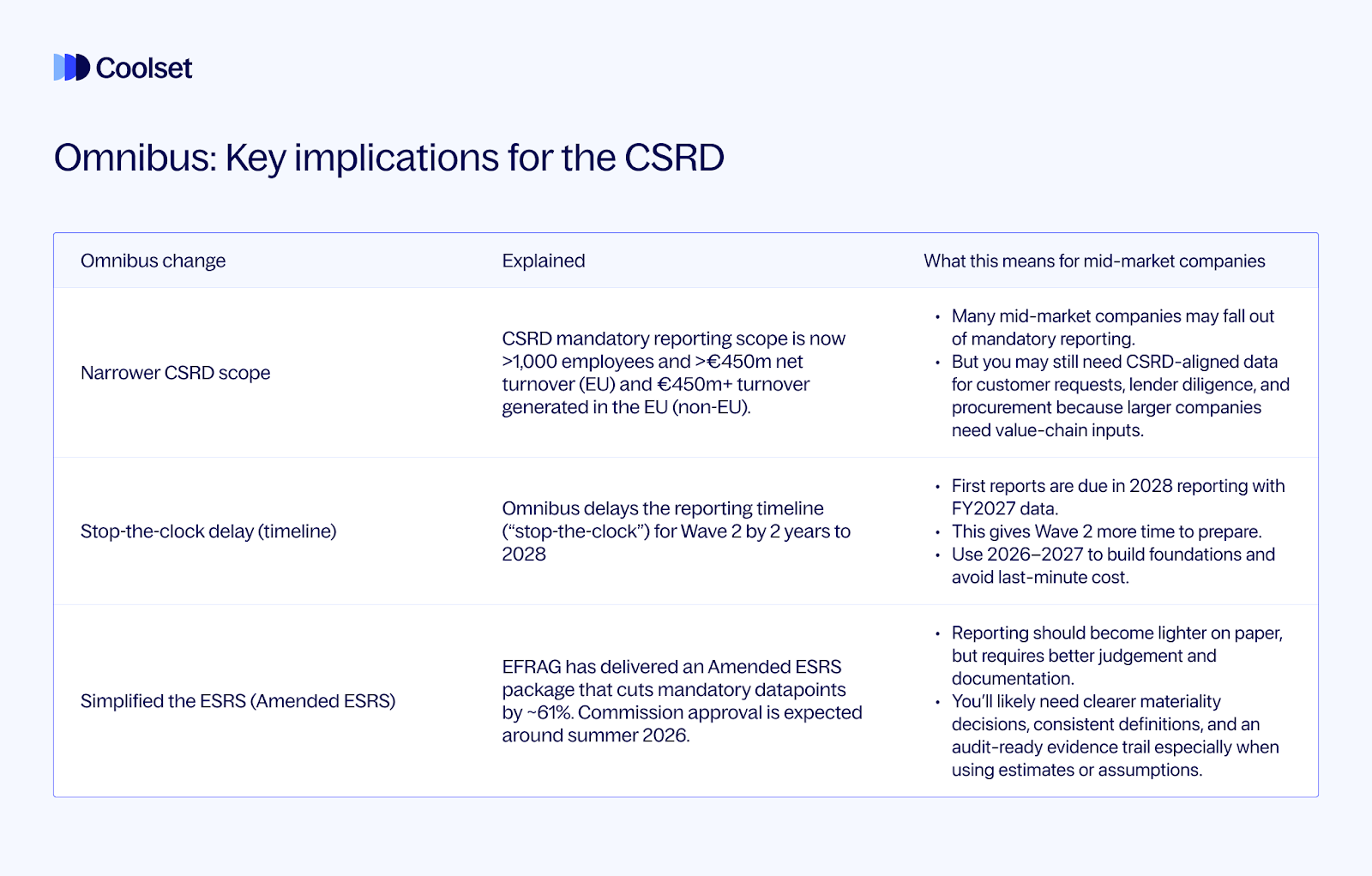

1) Omnibus narrows the scope of CSRD

Under the original CSRD design, the directive expanded reporting far beyond the old NFRD, capturing many large companies and listed mid-market companies based on thresholds such as 250+ employees and turnover/asset criteria.

Omnibus shifts that direction by proposing a significantly narrower scope, focusing on the largest undertakings. The most widely communicated outcome (as of late 2025) is that CSRD will likely apply primarily to companies above a higher employee threshold (e.g., 1,000+ employees) and greater than €450m net turnover, meaning many mid-market companies may fall out of mandatory scope.

What this means:

- Some companies that were preparing for CSRD based on the original criteria may no longer be required to report (depending on final adoption and national implementation).

- However, even out of scope companies may need to be able to share auditable sustainability metrics (especially emissions and workforce data) in RFPs, financing reviews, and supplier assessments.

2) Omnibus delays the reporting timeline (“stop-the-clock”) for wave 2

Omnibus is also associated with the legally adopted “stop-the-clock” approach which pushed back the CSRD reporting deadlines for companies that were meant to enter the regime in Wave 2 and Wave 3 by two years.

The practical effect was that many companies received two additional years before their first required CSRD report.

3) Omnibus triggers a rewrite of ESRS (simplified “Amended ESRS”)

The third major Omnibus effect is the push to simplify the ESRS. In response, the body advising the European Commission on sustainability reporting standards, EFRAG has delivered a streamlined Amended ESRS set designed to reduce reporting burden by cutting mandatory datapoints substantially.

This does not eliminate the ESRS, it changes how companies will likely report once the revised standards become law. The direction of travel is:

- Fewer mandatory datapoints (61% under the final EFRAG updates)

- More emphasis on clear judgement (especially around materiality)

- Stronger alignment with global frameworks like IFRS S1/S2 and the GHG Protocol

- More flexibility in estimates and aggregation, but also stronger expectations for quality and “fair presentation”.

At Coolset we are tracking the Omnibus reforms. See the Coolset Academy for the latest CSRD and ESRS updates.

Read our detailed breakdown of the Amended ESRS here.

Which companies are in-scope for CSRD after Omnibus?

As of January 2026, Wave 1 is already reporting under CSRD, and future scope is expected to narrow to the largest companies (1,000+ employees and €450m+ turnover), subject to final legal adoption.

For most mid-market companies, the key question is what scope will apply once the Omnibus reforms are fully finalized.

Important: The thresholds are pending final Commission adoption and publication, but they are effectively approved as there has been alignment between the Commission, Parliament and Council in trilogue discussions.

What does this mean for companies below the compliance thresholds?

If your company is below 1,000 employees or below €450m turnover, you are unlikely to be legally required to publish a CSRD report if the Omnibus scope changes are adopted as currently agreed.

However, many companies may still face CSRD-aligned requests from customers, lenders, and procurement, especially for emissions data, transition planning, and workforce metrics, because larger companies need value-chain data for their own reporting and risk processes.

What are the CSRD reporting requirements in 2026 and onward?

The CSRD requires in-scope companies to publish a structured sustainability statement as part of their annual reporting that is standardized and auditable.

What you disclose is defined through the ESRS and determined through double materiality, meaning you report both:

- how sustainability issues affect the business and,

- how the business impacts people and the environment.

Below are the core CSRD reporting requirements in practice.

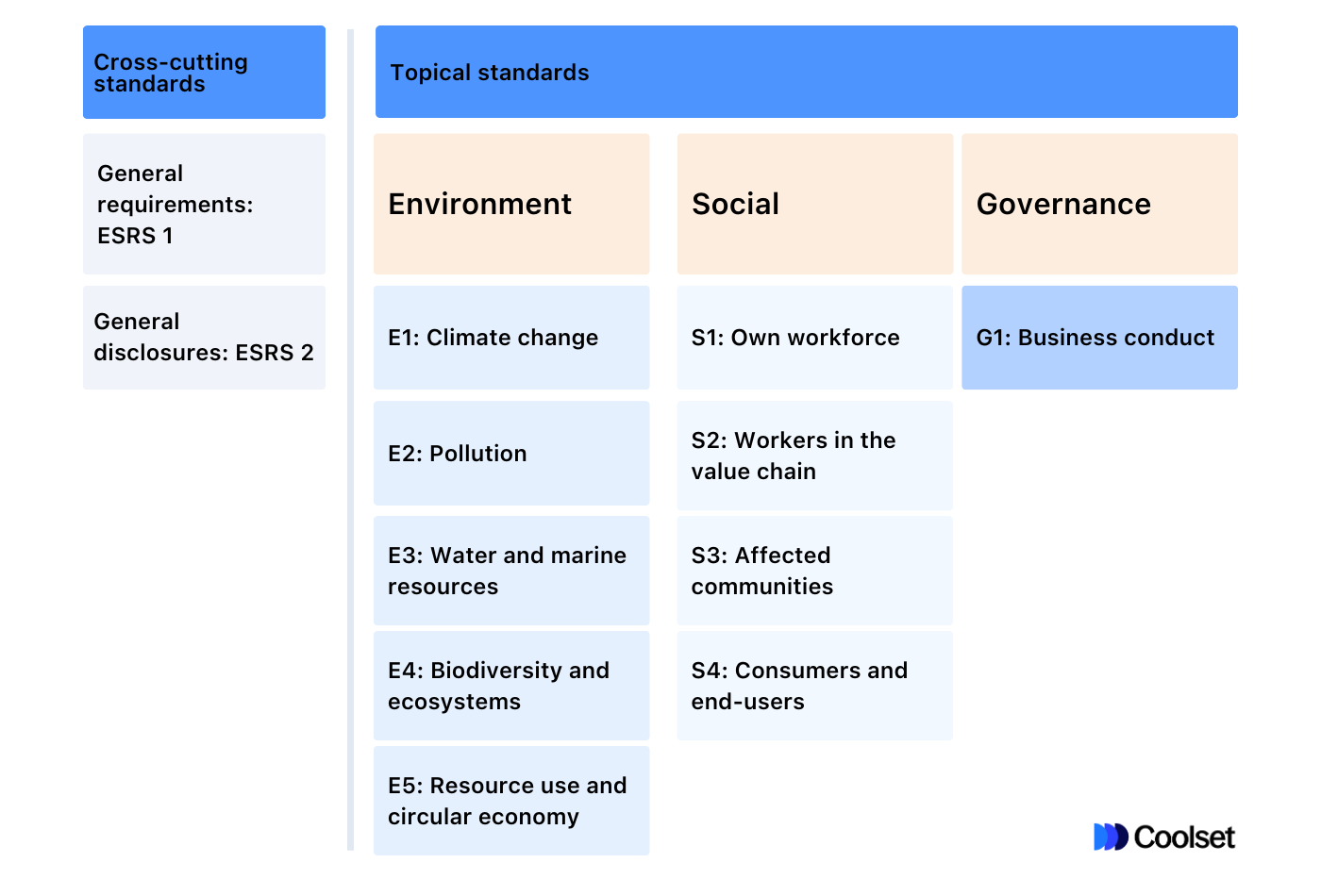

Report using ESRS: guided by materiality

CSRD reporting is structured around the ESRS, which include general disclosures (ESRS 1 and 2) that apply to all companies and topic-specific standards (E1-E5, S1-S4 and G1) you report on if they are material for your business.

Under the Amended ESRS, you start by deciding what topics are material, and you only report the detailed topical disclosures for those topics. That makes a defensible materiality assessment one of the biggest drivers of reporting effort.

Use this chart to see how the ESRS is organized:

Conduct and document a double materiality assessment (DMA)

Companies must run a double materiality assessment and use it to determine which ESRS disclosures apply. Under the Amended ESRS, the DMA is intended to be more workable, with clearer steps and a cleaner distinction between material and non-material topics, including more flexibility in how you structure the assessment.

Disclose strategy, governance, policies, actions and targets

CSRD reporting is not limited to KPIs. Companies also need to explain how sustainability is governed and managed, typically covering board/management oversight, strategy and resilience, policies and due diligence, actions and resources, targets, and progress.

For mid-market teams, this is often the hidden workload: even if the data exists, it still needs a consistent narrative, clear ownership, and supporting evidence that can stand up to assurance.

Apply proportionality + reliefs (estimates and value-chain data)

A major practical shift under the Amended ESRS direction is more proportionality. This includes broader use of estimates where exact data isn’t available, and reduced pressure to obtain certain value-chain data where it would be undue cost or effort, alongside reliefs in areas like anticipated financial effects and M&A timing.

In practice, companies are not expected to have perfect value-chain data immediately. But they do need a reasonable approach, transparent assumptions, and documentation for estimates.

Align with global frameworks and GHG Protocol where relevant

The Amended ESRS move closer to global reporting approaches, including IFRS S1 and S2 for transition plans, scenario analysis and financial effects, and explicit alignment with the Greenhouse Gas Protocol for emissions reporting.

This can reduce duplication for companies reporting across multiple frameworks, but it still requires clear mapping and consistent definitions.

Meet assurance and digital reporting requirements

CSRD introduces mandatory assurance (starting with limited assurance) and requires sustainability information to be published in a digitally usable format.

In practice, assurance readiness depends on evidence: clear data owners, traceable sources, and documented methodologies are critical, especially as materiality decisions and estimates become more central under the Amended ESRS direction.

How to prepare for CSRD in 2026?

The Omnibus package has already confirmed a delayed timeline for Wave 2 and a narrower CSRD scope agreed in trilogue, so companies should treat the new thresholds as the working baseline. The remaining moving piece is the Amended ESRS, which is expected to be finalized via Commission approval around summer 2026.

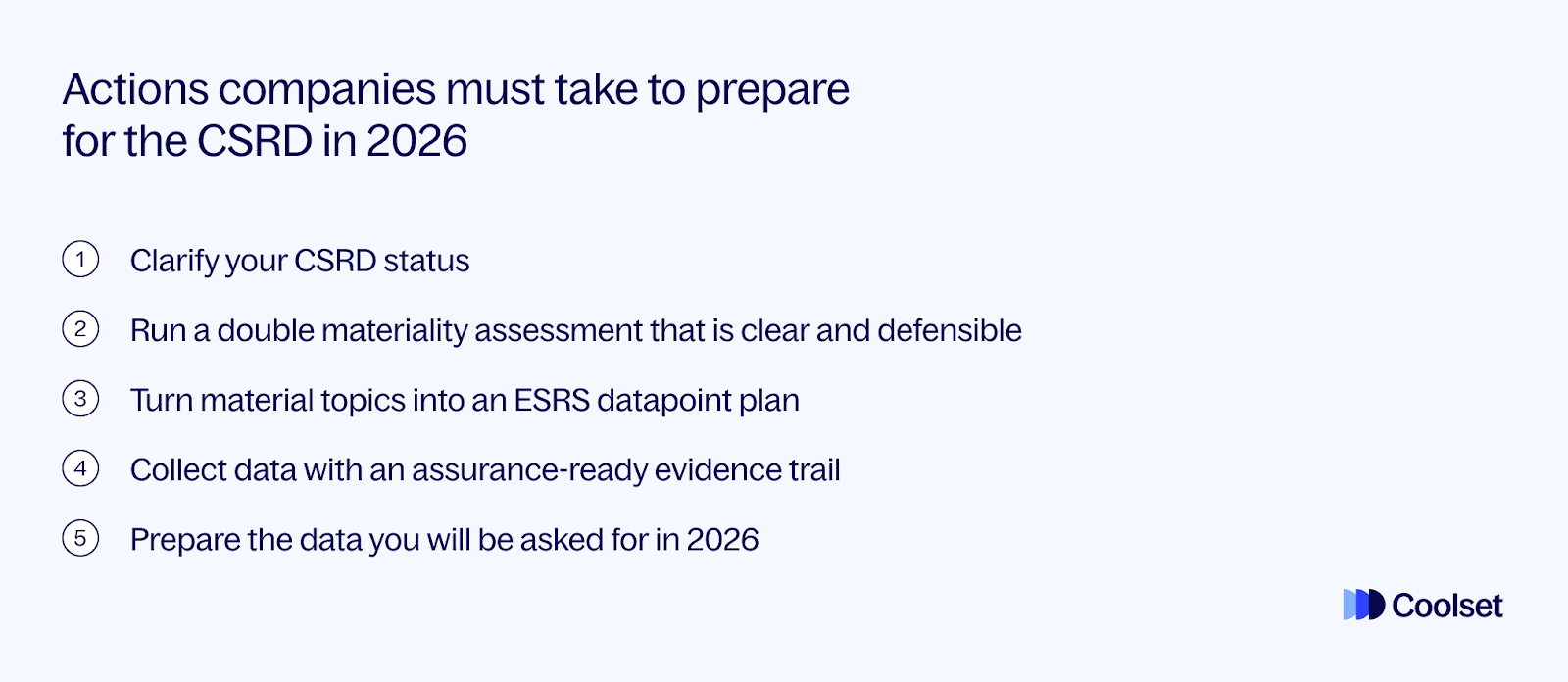

A practical 2026 CSRD preparation plan looks like this:

1) Clarify your CSRD status

Work out which bucket you are in and write it down internally:

- Already reporting (Wave 1)

- Expected to report later (Wave 2, with the delayed start date)

- Not expected to report under the new Omnibus scope (based on the 1,000+ employees and €450m+ turnover baseline)

Once you know your status, set the right level of effort for 2026: full reporting readiness for Wave 2, or a smaller track focused on the data customers and banks may request.

2) Run a double materiality assessment that is clear and defensible

Materiality is becoming the main filter under the Amended ESRS, so this is the most valuable work you can do in 2026. Keep it simple and defensible:

- list your main impacts, risks and opportunities

- score them consistently

- involve Finance, Procurement and HR early

- document why topics are in or out (i.e. material or not)

3) Turn material topics into an ESRS datapoint plan

Do not try to collect everything. Create a focused list of disclosures that match your material topics:

- list the ESRS datapoints you expect to report

- assign an owner for each datapoint

- note where the data lives today (system, team, supplier)

- set a collection frequency that matches your reporting cycle

Learn more on how to prepare for the Amended ESRS here.

Get access to Coolset’s ESRS cheatsheet. It shows how datapoints are structured across standards, articles and paragraphs, and is designed to help sustainability, ESG and compliance teams understand the scope and complexity of CSRD reporting for 2026.

4) Collect data with an assurance-ready evidence trail

Assurance depends on proof, not just numbers. For every datapoint you collect, capture:

- source files or system exports

- calculation method and assumptions

- whether it is measured or estimated

- who reviewed and approved it

If you do this continuously, assurance becomes a review exercise instead of a last minute scramble.

5) Prepare the data you will be asked for in 2026

Even if you are not publishing a CSRD report soon, you will likely receive CSRD style requests from customers, banks and procurement. Prioritize the information that comes up most often:

- Scope 1 and 2 emissions, and how you calculate them

- a plan for Scope 3, including what you can estimate today

- key workforce metrics and relevant policies

- governance basics, including oversight and responsibilities

- a simple transition plan status update (even if incomplete)

This also makes you responsive to external requests and reduces the workload if you later fall in scope.

How can software help with CSRD compliance?

CSRD compliance is less about writing a report and more about running a repeatable process: deciding what’s material, assigning ESRS datapoints to owners, collecting data from across the business and suppliers, and storing evidence for assurance. Software replaces scattered spreadsheets with one workflow where tasks, data, and audit proof live together.

Here are some practical ways software supports CSRD/ESRS compliance:

- Turns ESRS into an, up-to-date, trackable compliance checklist: Break ESRS into concrete datapoints, filter by materiality, assign each disclosure to an owner, and track completion by entity and reporting year so you always know what’s done, what’s missing, and what’s next.

- Collects supporting evidence and secure assurance: Attach sources, calculations, methodologies, assumptions, and approvals to each datapoint in one place. When assurance begins, you can show exactly where each number came from, without rebuilding evidence at the end.

- Coordinates cross-functional input without chasing teams: CSRD data lives across Finance, HR, Operations, Procurement, Legal, and Sustainability. A shared workflow lets you assign tasks, set deadlines, request inputs, and follow progress, replacing email threads and scattered files.

- Makes double materiality defensible and repeatable: Structure IROs, apply scoring consistently, document decisions, and generate a clear “why in/why out” trail, which is critical as materiality becomes the central filter under the Amended ESRS.

- Helps manage value-chain gaps with documented estimates: Track supplier inputs, flag missing data, record estimates and assumptions, and document “reasonable and supportable” logic, so you can report even when value-chain data isn’t perfect.

With built-in workflows and evidence tracking, Coolset can help you stay CSRD-compliant without rebuilding your reporting process every year.

Request a free demo with our team to learn how you can run your materiality assessment, collect ESRS datapoints, and keep evidence audit-ready, all in one platform.

FAQs

Does CSRD apply to my company after the Omnibus changes?

Yes, if your group meets the new Omnibus CSRD scope (EU undertakings with >1,000 employees and >€450m net turnover, and non-EU groups with €450m+ turnover generated in the EU.

When do we need to start reporting under CSRD (what’s the updated timeline)?

Wave 1 companies are already reporting (first reports published in 2025 for FY2024). Under Omnibus and the adopted stop-the-clock delay, Wave 2 companies publish their first CSRD report in 2028, covering FY2027. Listed SMEs (the original Wave 3) are expected to be out of mandatory CSRD scope and instead encouraged to report voluntarily under the VSME standard.

What do we actually need to report under ESRS and what’s changing with the Amended ESRS?

CSRD reporting follows ESRS: cross-cutting disclosures plus topical ESG standards, based on double materiality. The Amended ESRS aim to reduce mandatory datapoints (by 61%) and clarify language, but they are expecting final approval. Expect fewer datapoints, but higher expectations for judgement and evidence.

What is double materiality, and how do we run a double materiality assessment for CSRD?

Double materiality means reporting both financial impacts on the business and impacts on people/environment. A CSRD-ready assessment maps key impacts, risks, and opportunities (IROs), evaluates severity and likelihood, and links results to ESRS disclosures. It should be documented, repeatable, and auditable.

If we’re not legally in scope, why are customers/banks still asking for CSRD-style data?

Because large companies and financial institutions must disclose value-chain impacts and risks. They’ll request supplier emissions, policies, workforce metrics, and transition data to meet their own reporting and risk requirements. Even out-of-scope companies benefit from having “CSRD-ready” data available.

What are the biggest CSRD reporting risks for mid-market companies (and how do we avoid them)?

The biggest risks are weak materiality logic, missing value-chain data, poor evidence trails, unclear ownership, and late assurance readiness. Avoid them by assigning datapoint owners early, documenting methodologies, collecting evidence as you go, and running internal reviews before external assurance begins.

Structured session to ensure your ESRS reporting is audit-proof

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

All the requirements around CSRD compliance summarized on one page

Download our CSRD cheat sheet for 2025 and save it for future use.

.webp)