ESRS S1 after Omnibus: own workforce reporting under the amended ESRS (2026)

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key Takeaways

- ESRS S1 is the CSRD standard for own workforce reporting, covering 16 disclosure requirements.

- The November 2025 EFRAG draft removes 61% of original datapoints and applies only when own workforce is deemed material.

- Key changes include defined turnover calculations, country-specific wage benchmarks, and mandatory gender pay gap reporting.

- Coolset's software streamlines ESRS S1 data collection to accelerate CSRD compliance.

ESRS S1 (Own workforce) sets the reporting requirements for how a company manages impacts, risks and opportunities related to employees and certain non-employee workers in its own workforce.

The original European Sustainability Reporting Standards (ESRS) were adopted by the European Commission in July 2023. They are the standards used by companies in scope of the Corporate Sustainability Reporting Directive (CSRD) to structure sustainability reporting and to define what to disclose on environmental, social and governance topics. After the Omnibus Proposal was published on February 26, 2025, EFRAG was tasked with simplifying the ESRS, resulting in a new draft version published in November 2025. All in all, 61% of original datapoints have been removed in the new version.

So what exactly is the new ESRS S1 and why is it essential? What are its primary requirements? And how can you effectively implement the datapoints? The article will give you a comprehensive understanding of the updated standard.

When is ESRS S1 material and what happens if parts are not?

ESRS S1 is one of the four social standards. It focuses on the company’s impacts on its own workforce, including working conditions, social dialogue, health and safety, training, diversity and equal treatment and other labor-related human rights.

ESRS S1 only applies if Own workforce is material, but some workforce data points still become mandatory once the topic is material.

Under CSRD, companies do not report every topic in every ESRS by default. A double materiality assessment determines whether own workforce is material and which sub-topics within ESRS S1 are material for reporting.

Two practical implications matter:

- If ESRS S1 is not material, the company does not report ESRS S1

- If ESRS S1 is material, the company reports ESRS S1, but may omit immaterial sub-topics (with a clear explanation)

In the November 2025 ESRS S1 draft, EFRAG also makes explicit that once own workforce is material, the disclosure on employee characteristics is required (S1-5). Disclosure on non-employees is required if non-employees are connected to material impacts, risks or opportunities (S1-6).

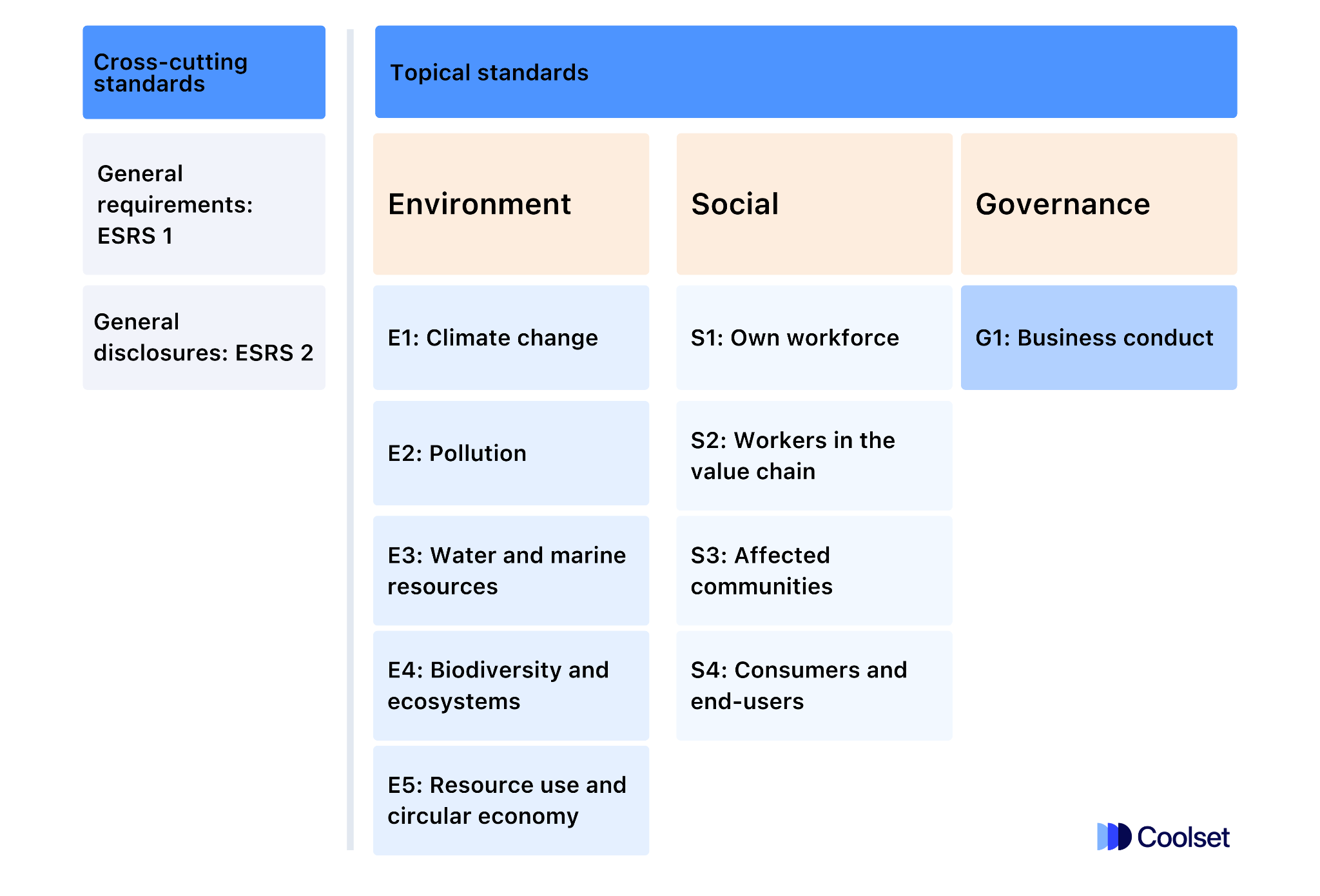

The following table lays out the structure of the ESRS:

What changed in the November 2025 draft?

The November 2025 draft tightens definitions and shifts ESRS S1 toward fewer, clearer data points that are easier to verify and compare.

If the draft direction sticks (which we think it will), the biggest practical changes for reporting teams are:

- Clearer employee breakdowns, including a defined approach for turnover calculation and required context on methodology (end-of-year vs average)

- A narrower diversity focus: gender distribution at top management level (age distribution drops out in the draft)

- Adequate wage reporting becomes more benchmark-driven and country-specific, with explicit disclosure of affected countries and shares when wages are not adequate

- Social protection reporting becomes an “exceptions” disclosure: name countries where employees lack coverage for specific major life events

- Health and safety reporting becomes more structured, including coverage of the occupational safety and health system, accident rates per one million hours worked and days lost

- Work-life balance reporting focuses on entitlement to family-related leave (not usage)

- Remuneration focuses on unadjusted gender pay gap and pay inequality via the highest-paid-to-median ratio, with tighter rules on what to include in pay

- Human rights and discrimination incidents are framed as substantiated incidents and require linking to financial statement amounts for fines, penalties and compensation

Important: this is a draft. Companies should track the final ESRS text, but the direction is already useful for building data collection processes that will survive scrutiny.

What changed in ESRS S1 after Omnibus: scope, materiality, disclosures?

After the Omnibus updates, ESRS S1 Own Workforce remains materiality-based, but it clarifies who is in scope, tightens when baseline workforce data must be reported, and reinforces expectations on engagement, grievance channels, and core workforce metrics.

Scope

ESRS S1 applies when impacts, risks or opportunities related to the undertaking’s own workforce are material. 'Own workforce' includes employees and certain non-employees who supply labour to the undertaking (such as self-employed contractors or agency workers). It does not cover workers in the upstream or downstream value chain (covered under ESRS S2).

Materiality

ESRS S1 continues to follow the double materiality approach, but it makes clearer that once 'own workforce' is considered material, companies are expected to disclose key baseline workforce information, especially employee characteristics, and to disclose non-employee information when those workers are connected to material impacts, risks, or opportunities.

Disclosures

Disclosure requirements continue to follow the standard ESRS structure (policies, actions/resources, targets, and metrics), with a strong focus on: how the undertaking manages workforce impacts; how it engages with workers and their representatives; whether workers have channels to raise concerns and access remedy; and consistent quantitative reporting on workforce composition and key working-conditions metrics (such as wages, social protection, health and safety, training, diversity and pay, and incidents of discrimination or other human rights issues).

Impacts, risks and opportunities management

ESRS S1 expects a company to explain how it governs own workforce impacts, risks and opportunities through policies, engagement, remediation and actions.

What needs to be disclosed under S1-1 policies related to own workforce?

Companies must describe policies used to manage material impacts, risks and opportunities related to own workforce and whether policies cover the whole workforce or specific groups. The draft also explicitly asks whether policies address trafficking in human beings, forced labor and child labor.

What to include in practice:

- Which workforce groups the policy covers (all employees, a geography, a factory, self-employed people)

- How the policy is communicated and who is expected to implement it (often employees, contractors, suppliers)

- Whether policies explicitly cover trafficking, forced labor and child labor

What needs to be disclosed under S1-2 engagement, grievance channels and remediation?

Companies must explain how they engage with employees or worker representatives, how workforce perspectives inform decisions and which channels exist for workers to raise concerns and obtain remedy.

New or clearer draft expectations to call out:

- Explain how the company gains insight into perspectives of vulnerable or marginalized groups, when the company takes action to do so (examples include women, migrants, people with disabilities)

- Disclose global framework agreements or other outcomes reached with worker representatives if they exist

- State whether a grievance mechanism exists and explain how the company assesses channel effectiveness

- Describe the general approach to remediation when the company caused or contributed to a material negative impact

What needs to be disclosed under S1-3 actions and resources?

Companies must describe key actions and resources used to manage material impacts, risks and opportunities and how effectiveness is tracked.

The draft adds useful specificity:

- Actions must cover prevention, mitigation and remediation of material negative impacts

- Explain how effectiveness is tracked, unless already covered via ESRS 2 tracking or metrics disclosures

- Explain what the company does when workforce actions conflict with other business pressures

{{custom-cta}}

Metrics and targets

What needs to be disclosed under S1-4 targets related to own workforce?

Companies must disclose qualitative and/or quantitative targets related to own workforce under the ESRS 2 target framing.

In practice, targets work best when they are:

- Time-bound

- Outcome-oriented (not just activity-based)

- Tied to the material impacts and risks identified in the double materiality assessment

What do companies need to report under S1-5 employee characteristics?

Companies must disclose core employee workforce numbers and turnover, plus explain methodology choices if needed.

New or updated data points to make explicit:

- Total number of employees (headcount)

- Break down by gender

- Break down by country for countries with 50+ employees that are also in the top ten by employee count

- Total number of employees (headcount or FTE) by contract type

- Permanent employees, by gender

- Temporary employees, by gender

- Non-guaranteed hours employees (no gender breakdown required in the table template)

- Employee turnover rate for the reporting period

- Draft defines turnover as leavers (voluntary or due to dismissal, retirement or death in service) divided by average employee headcount

- Qualitative explanation if employee numbers differ between this disclosure and the most representative number in financial statements

- Methodology context for how employee data is compiled (end-of-year vs average)

Practical note for EU companies with multiple countries: use national legal definitions for permanent, temporary and non-guaranteed hours at country level, then add up totals.

What do companies need to report under S1-6 non-employee characteristics?

Companies must disclose the total number of non-employees in the own workforce if non-employees are connected to material impacts, risks or opportunities.

The draft frames when this becomes relevant:

- Non-employees are critical to the business model (flexible labor, core processes)

- Reliance on non-employees is increasing and may create risk

- Non-employees represent a substantial share of the workforce and impacts are material for this group

The total number can be headcount or FTE, reported at end-of-year or as an average, but the company must state which option it used.

What do companies need to report under S1-7 collective bargaining and social dialogue?

Companies must report collective bargaining coverage and, in EEA countries with significant employment, social dialogue coverage via worker representatives.

New or clearer breakdown requirements:

- Percent of total employees covered by collective bargaining agreements

- In the EEA

- Whether there are one or more collective bargaining agreements

- For each “significant employment” EEA country (those already disclosed under S1-5 country breakdown), percent of employees covered

- Outside the EEA

- Percent of employees covered by collective bargaining agreements by region

- Social dialogue in EEA countries

- Percent of employees covered by workers’ representatives per significant-employment country

- Whether the company has agreements for a European Works Council (or similar bodies)

What do companies need to report under S1-8 diversity?

Companies must disclose gender distribution at the top management level, both as headcount and percentage.

The draft defines “top management” as the two levels below administrative and supervisory bodies, unless a company uses a different definition and discloses it.

What do companies need to report under S1-9 adequate wages?

Companies must disclose whether employees are paid an adequate wage and which benchmark is used, with country-level context. If not all employees are paid an adequate wage, companies must name the countries and the percentage of employees concerned.

New or clearer draft mechanics:

- The calculation uses the lowest wage among employees in each country (excluding interns and apprentices)

- Lowest wage means basic wage plus fixed additional payments guaranteed to all employees

- The adequate wage benchmark cannot be lower than

- In the EU, the wage level from collective bargaining or the statutory minimum wage set under the EU adequate minimum wages directive

- Outside the EU, an adequate minimum wage that provides a decent standard of living (confirmed in line with ILO living wage principles) or a living wage estimate that takes ILO principles into account

What to write in the article section so it stays actionable:

- State the benchmark used per country (collective agreement, statutory minimum wage, living wage estimate source)

- Explain how lowest wage was identified

- If gaps exist, list countries and affected employee shares

What do companies need to report under S1-10 social protection?

Companies must disclose countries where employees lack social protection for major life events, if gaps exist.

The draft is explicit about which events matter:

- Sickness

- Unemployment (starting from when the employee is working for the company)

- Employment injury and acquired disability

- Maternity leave

This is an “exceptions” disclosure. If all employees are covered, a company can usually say so with brief context on coverage sources (public schemes, company benefits, collective bargaining).

What do companies need to report under S1-11 persons with disabilities?

Companies must disclose the percentage of employees with disabilities, subject to legal restrictions on data collection.

The draft also expects methodological transparency:

- Explain the definition used (national definitions or a consistent company definition across countries)

- Explain data sources (voluntary surveys, mandatory quota reporting)

What do companies need to report under S1-12 training and skills development?

Companies must disclose two core metrics for the reporting period.

New or updated data points:

- Percent of employees who participated in formalized performance and career development reviews

- Average number of training hours per employee

The draft clarifies that a formalized review is based on criteria known to the employee and undertaken at least once per year.

What do companies need to report under S1-13 health and safety?

Companies must disclose coverage of the occupational safety and health (OSH) management system and a structured set of incident metrics.

New or clearer draft data points to make explicit:

- Percent of own workforce covered by the OSH management system (headcount basis), based on legal requirements and/or recognized standards

- Fatalities

- Sum of fatalities from recordable work-related accidents among all people in own workforce and also workers on company sites who are not part of own workforce

- Fatalities from recordable work-related ill health among employees

- Recordable work-related accidents

- Number of cases

- Rate of cases per one million hours worked

- Recordable work-related ill health among employees (number of cases), subject to legal restrictions

- Days lost due to recordable work-related accidents and ill health among employees

If non-employees are material under S1-6, the company must include non-employee cases in fatalities from accidents and accident cases and break down between employees and non-employees where applicable.

What do companies need to report under S1-14 work-life balance?

Companies must disclose the percentage of employees entitled to family-related leave during the reporting period.

Family-related leave includes:

- Maternity leave

- Paternity leave

- Parental leave

- Carers’ leave

The focus is entitlement, not uptake.

What do companies need to report under S1-15 remuneration?

Companies must disclose:

- Unadjusted gender pay gap (difference in average pay levels between female and male employees as a percentage of male employees’ average pay)

- Annual total remuneration ratio of the highest-paid individual to median annual total remuneration for all employees (excluding the highest-paid individual)

The draft is unusually specific about inclusions:

- Gender pay gap should include all male and female employees and include ordinary basic salary plus other remuneration made available to all employees, cash or in-kind

- The ratio includes base salary and, depending on policy, variable pay, cash allowances, bonuses, commissions, profit-sharing, benefits in-kind (cars, insurance, wellness) and long-term incentives at fair value

What do companies need to report under S1-16 discrimination and other human rights incidents?

Companies must disclose three things for the reporting period:

- Number of incidents of discrimination at work (including harassment), subject to privacy regulations

- Number of other human rights incidents connected to own workforce (excluding discrimination), subject to privacy regulations

- Total amount of fines, penalties and compensation for damages recognized in financial statements for these incidents

The draft clarifies that incidents are substantiated instances such as judicial or non-judicial proceedings initiated or incidents registered by the company through internal processes.

How should companies implement ESRS S1 without drowning in HR data?

A good ESRS S1 approach starts with a clear materiality decision, then builds a data model that matches the disclosure requirements instead of collecting everything “just in case.”

1. Conduct a double materiality assessment

Companies are not required to report on all 37 sub-topics described in the topical ESRS, only those that are material to their business. Conducting a double materiality assessment helps identify and prioritize the most significant ESG matters to report on.

This process should consider both impact materiality and financial materiality when identifying material matters.

Examples

Enel has included ‘Own workforce’ as a material issue in their sustainability report. Their focus is on ensuring a safe, inclusive, and empowering work environment, which they see as directly tied to their overall business performance and sustainability goals. They list the ‘health and safety of employees’ and ‘quality of corporate life’ as key components of their material topics.

Nestlé has recognized ‘Own workforce’ as material in their CSRD-aligned reporting. Their focus on employee rights, diversity, inclusion, and working conditions is central to their approach to sustainability, particularly given the extensive workforce required in their global operations.

Below each ESRS sit sub-topics, which inform the areas that the materiality assessment should cover. The amount of sub-topics vary depending on the ESRS, but there are generally between 3 and 5. When conducting a materiality assessment for ESRS S1, consider the following subtopics:

Sub-topic 1: Working conditions

Evaluates the quality of the working environment provided by the company, including health and safety measures, work-life balance, fair remuneration, and access to social security benefits. This ensures the company fosters a safe, healthy, and supportive workplace for all employees.

Sub-topic 2: Equal treatment and opportunities for all

Focuses on the company’s commitment to diversity, equity, and inclusion (DEI). This includes measures to address pay gaps, prevent discrimination, support employees with disabilities, and ensure equal opportunities regardless of gender, race, or other personal characteristics. This helps identify areas for improving DEI practices.

Sub-topic 3: Other work-related rights

Assesses the company’s policies and practices related to broader work-related rights, such as freedom of association, collective bargaining, and privacy at work. It also includes how the company handles grievances and complaints related to these rights, ensuring these rights are respected is crucial for maintaining a fair and just workplace.

2. Tackle key elements in the workforce management plan

ESRS S1 requires businesses to provide a detailed account of their workforce management plan, which is a corporate action plan to ensure fair and sustainable labor practices.

Key elements of a workforce management plan include:

- Establishing clear workforce policies and targets.

- Identifying and implementing measures to improve workforce conditions with quantifiable goals.

- Securing financing for workforce initiatives.

- Embedding the workforce plan in your overall business strategy and financial planning.

- Obtaining approval from the board.

- Aligning the plan with risk management and integrating it into the governance framework.

3. Create an action plan guiding workforce management

Detail the specific steps your business will take to enhance workforce management, including:

- Implementing sustainable practices: Outline actions like improving working conditions, enhancing employee benefits, or fostering a diverse workplace.

- Stakeholder engagement: Describe how you will involve employees, unions, and other stakeholders in your workforce management efforts.

4. Set clear goals for workforce development and well-being

Your action plan should include specific, measurable goals for improving workforce development and well-being. Set ambitious yet achievable targets to ensure continuous improvement.

5. Track and disclose workforce metrics

Monitor and report on key workforce metrics for transparency and to identify areas for improvement. Track metrics such as employee turnover, health and safety incidents, and training participation rates.

6. Report workforce policies and practices

Under ESRS S1, businesses must disclose their workforce policies and practices in detail. Report on health and safety measures, diversity and inclusion initiatives, and employee development programs.

Select the right software for workforce reporting

For businesses reporting on CSRD, managing workforce topics under ESRS S1 can be daunting and time-consuming, especially when data sits across HR, finance and H&S systems. The right tools can make a significant difference. Workforce reporting software can simplify the process, streamline data collection and analysis, provide actionable insights and generate reports automatically, accelerating your compliance journey.

Discover how workforce reporting software can fast-track your CSRD compliance by requesting a free demo today.

FAQ

Does ESRS S1 apply to contractors and freelancers?

ESRS S1 covers employees and certain non-employees in the company’s own workforce, such as self-employed people supplying labor or workers provided by employment agencies. ESRS S1 does not cover upstream or downstream value chain workers, those are covered under ESRS S2.

What is new in S1-5 employee characteristics in the November 2025 draft?

The draft explicitly requires headcount by gender and by key countries, contract type breakdowns, employee turnover and a description of the methodology used to compile employee data (end-of-year vs average).

How is employee turnover calculated in the draft?

The draft defines employee turnover as the number of employees who leave voluntarily or due to dismissal, retirement or death in service divided by the average employee headcount.

What does ESRS S1 mean by adequate wages?

The draft asks whether employees are paid an adequate wage and which benchmark is used, with country-level context. The benchmark cannot be lower than applicable minimum wage levels in the EU or credible living wage or adequate minimum wage references outside the EU.

What needs to be disclosed on social protection?

If gaps exist, companies must name countries where employees lack social protection for sickness, unemployment, employment injury and acquired disability or maternity leave.

What are the remuneration metrics in ESRS S1?

The draft requires an unadjusted gender pay gap and the ratio of the highest-paid individual’s annual total remuneration to median annual total remuneration for employees (excluding the highest-paid individual), with clear rules on what pay components to include.

Understand EFRAG's amended datapoints, materiality and audit-ready reporting

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

Get your CSRD compliance suite

Streamline data collection and reporting across the Double Materiality Assessment and ESRS topic disclosures.

.webp)