ESRS S2 after Omnibus: workers in the value chain reporting under the amended ESRS (2026)

.webp)

Disclaimer: New EUDR developments - December 2025

In November 2025, the European Parliament and Council backed key changes to the EU Deforestation Regulation (EUDR), including a 12‑month enforcement delay and simplified obligations based on company size and supply chain role.

Key changes proposed:

- New enforcement timeline: 30 December 2026 for large/medium operators, 30 June 2027 for small/micro operators

- Simplified DDS: One-time declarations for small and micro primary producers

- Narrowed scope: Most downstream actors and non‑SME traders would no longer need to submit DDSs

- New DDS requirement: Estimated annual quantity of regulated products must be included

These updates are not yet legally binding. A final text will be confirmed through trilogue negotiations and formal publication in the EU’s Official Journal. Until then, the current EUDR regulation and deadlines remain in force.

We continue to monitor developments and will update all guidance as the final law is adopted.

Key Takeaways

- ESRS S2 applies under CSRD only when value chain workers are identified as material through the double materiality assessment.

- EFRAG's November 2025 amended draft introduces an explicit datapoint requiring disclosure of substantiated human rights incidents involving value chain workers.

- Map existing policies to ESRS S2's datapoints on forced labor, trafficking and child labor.

- Coolset's CSRD product helps structure ESRS S2 disclosures with guided templates and centralized evidence management for audit-ready reporting.

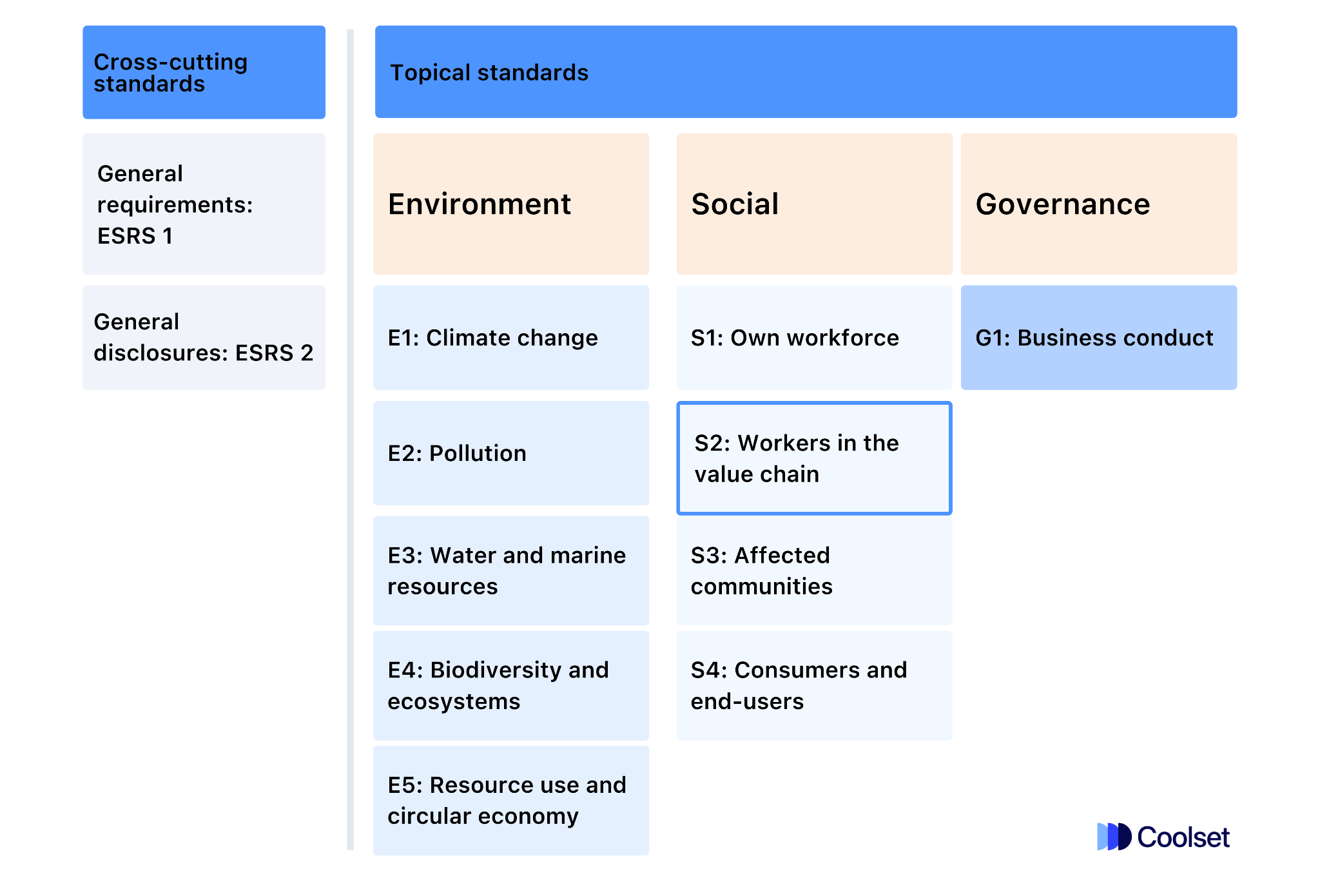

What is ESRS S2 and when does it apply?

EFRAG published a draft set of Amended European Sustainability Reporting Standards (ESRS) in November 2025 after the Omnibus proposal, with the goal of cutting the reporting burden. While these provide much needed clarity on the direction of reporting, it’s important to note that the revised standards are not legally binding yet and still require adoption by the European Commission, expected in summer 2026.

ESRS S2 is a topical standard under the social standards section of the ESRS. S2 sets the disclosure requirements for how companies report on workers in the value chain under the Corporate Sustainability Reporting Directive (CSRD). It applies to companies in scope for CSRD that identify that identify workers in the value chain as a material topic through their double materiality assessment.

It covers material impacts, risks and opportunities connected to workers outside a company’s own workforce, including workers employed by suppliers, contractors, outsourced service providers and downstream business relationships.

To learn more about the CSRD, who is in scope and how the Omnibus affects scope, timing and requirements, read more here.

What changed in ESRS S2 after Omnibus: scope, materiality, disclosures

Following the Omnibus push to streamline sustainability reporting, the amended ESRS S2 draft tightens scope and disclosures to what’s materially relevant for value chain workers.

Companies should expect fewer checklist-style datapoints and more focus on whether worker-related risks exist in the value chain, whether impacts are severe or systemic, and whether grievance and remediation mechanisms actually work. The draft also introduces an explicit datapoint requiring disclosure of material human rights incidents connected to value chain workers.

Read our full EU Omnibus Q&A article here

What does workers in the value chain mean under ESRS S2?

ESRS S2 covers workers in upstream and downstream value chains who are not part of the company’s own workforce.

Examples include:

- Outsourced workers operating on-site, such as catering or security staff

- Supplier workers producing goods using supplier work methods

- Maintenance workers from equipment providers working under contract

- Workers deeper in supply chains extracting raw materials used in products

This scope matters because many of the most severe labor-related risks sit outside direct employment structures.

What topics does ESRS S2 require companies to assess?

ESRS S2 focuses on impacts connected to labor and human rights across the value chain.

The standard lists six core sub-topics:

- Working conditions (wages, working time, job security, social protection)

- Freedom of association and collective bargaining

- Health and safety

- Training and skills development

- Diversity and equal treatment

- Other labor-related human rights, including child labor and forced labor

The draft updates clarify that companies only need to report on sub-topics that are material to the business.

{{custom-cta}}

Impacts, risks and opportunities management

ESRS S2 requires companies to explain how they identify and manage material impacts, risks and opportunities connected to workers in the value chain. This includes workers employed by suppliers, contractors and other business partners upstream or downstream.

Reporting only applies where these impacts are material under the double materiality assessment, and disclosures should focus on the areas where risks to workers are real, severe or systemic rather than generic statements.

What needs to be disclosed under ESRS S2-1 on policies relating to workers in the value chain?

Companies must describe policies for managing material impacts, risks and opportunities related to workers in the value chain.

Policies should explain:

- Which workers are covered (all value chain workers or specific groups)

- How policies address trafficking, forced labor and child labor

- Whether a supplier code of conduct exists

The amended draft makes these datapoints explicit:

- Trafficking in human beings

- Forced or compulsory labor

- Child labor

- Supplier code of conduct

In practice, companies should map existing human rights and procurement policies directly to ESRS S2 rather than rewriting everything from scratch.

What needs to be disclosed under ESRS S2-2 on engagement with workers in the value chain, existence of channels for workers in the value chain to raise concerns or needs and approaches to remedy?

ESRS S2-2 focuses on how companies engage with workers in the value chain and whether workers can raise concerns safely.

Companies must disclose:

- How engagement happens directly or through representatives or credible proxies

- How worker perspectives inform business decisions

- How companies gain insight into vulnerable or marginalized workers, such as migrant workers or workers with disabilities

Companies must also describe grievance channels, including whether a grievance mechanism exists.

The amended draft points companies toward the UN Guiding Principles effectiveness criteria (Principle 31) when assessing grievance channel quality.

A grievance mechanism is only meaningful if workers trust it and retaliation protections exist.

What needs to be disclosed under ESRS S2-3 on actions and resources related to workers in the value chain?

Companies must describe key actions and resources used to manage material impacts on workers in the value chain.

Disclosures should include:

- Actions taken or planned to prevent, mitigate or remediate harm

- How companies respond when tensions arise between worker protection and procurement or sales pressures

- How effectiveness is tracked over time

Actions should connect directly to the company’s leverage in the value chain.

For example, a company sourcing textiles might disclose:

- Supplier audit redesign

- Purchasing practice changes

- Collective action through industry initiatives

- Remediation programs for excessive working hours

New datapoint: What needs to be disclosed about human rights incidents?

A key new datapoint in the amended ESRS S2 draft is the requirement to disclose human rights incidents connected to value chain workers when material.

Incidents include substantiated cases such as:

- Judicial proceedings

- Complaints to OECD National Contact Points

- Incidents registered internally through company processes

Companies are not expected to list every case individually. Aggregation by incident type or worker group is allowed.

Severity drives materiality: companies focus primarily on the seriousness of impacts on workers.

Metrics and targets

The amended ESRS S2 draft reduces emphasis on broad mandatory metrics and instead focuses on targets and tracking that reflect the company’s material impacts on workers in the value chain. Metrics and targets should support assessment of whether policies, engagement and actions are delivering meaningful outcomes, particularly in high-risk parts of the supply chain.

What needs to be disclosed under ESRS S2-4 targets related to workers in the value chain?

Companies must disclose qualitative or quantitative targets related to workers in the value chain where relevant.

Targets should connect clearly to:

- Engagement outcomes

- Tracking effectiveness

- Improvements in worker impact management

For many companies, meaningful targets may relate to:

- Supplier grievance uptake

- Reduction of severe incidents

- Coverage of high-risk supply chain tiers

What should companies do next to prepare for ESRS S2 reporting?

Companies should prepare early for reporting under the Amended ESRS S2 framework:

- Start with the double materiality assessment: Workers in the value chain disclosures apply only when impacts, risks or opportunities are material. Document reasoning clearly.

- Map existing policies to the new explicit datapoints: Confirm whether policies address forced labor, trafficking, child labor and whether a supplier code of conduct exists.

- Review grievance mechanisms realistically: A grievance channel that exists on paper but fails in practice will not meet expectations.

- Prepare for human rights incident disclosure: Companies should build internal processes for identifying, substantiating and aggregating incidents based on severity.

- Prioritize relevance over completeness: Avoid defensive reporting. Focus on where the business model creates real worker-related risks.

How to use software to help reporting on pollution

Software makes ESRS S2 reporting more manageable by turning fragmented supplier and workforce data into structured disclosures.

A practical value chain worker reporting system should support:

- Mapping suppliers and outsourced workers by risk exposure

- Linking worker impacts to ESRS S2 datapoints

- Managing grievance mechanism evidence and remediation tracking

- Documenting incidents and severity filters consistently

- Producing audit-ready disclosures without manual rework

At Coolset, worker reporting becomes part of a broader sustainability data foundation, not a one-off compliance exercise.

{{product-tour-injectable}}

FAQs

Is ESRS S2 mandatory for every company reporting under CSRD?

No. Companies report under ESRS S2 only if workers in the value chain represent a material topic under the double materiality assessment.

Does ESRS S2 apply to a company’s own employees?

No. ESRS S2 covers workers outside the company’s own workforce. Employees fall under ESRS S1.

Do companies need a grievance mechanism for value chain workers?

Companies must disclose what channels exist for workers in the value chain to raise concerns, including whether a grievance mechanism is in place.

What is the new human rights incident datapoint in ESRS S2?

The amended draft requires disclosure of substantiated human rights incidents involving value chain workers, including judicial proceedings or internally registered cases.

Do companies need quantitative targets under ESRS S2?

Not always. ESRS S2-4 allows qualitative or quantitative targets depending on what is material and useful for tracking effectiveness.

Learn ESRS datapoints you can lock in today versus what to keep flexible until the final Delegated Act is published

on mobile screens

to experience this demo.

↘ Check if your documentation meets PPWR requirements

This free compliance checker scans your packaging documentation and maps it against mandatory PPWR data requirements, giving you a clear view of your compliance status. Get actionable insights on documentation gaps before they become compliance issues.

.webp)